During a week of much political news, economic data pointed to stability. Here are the 5 things we learned from U.S. economic data released during the week ending November 11.

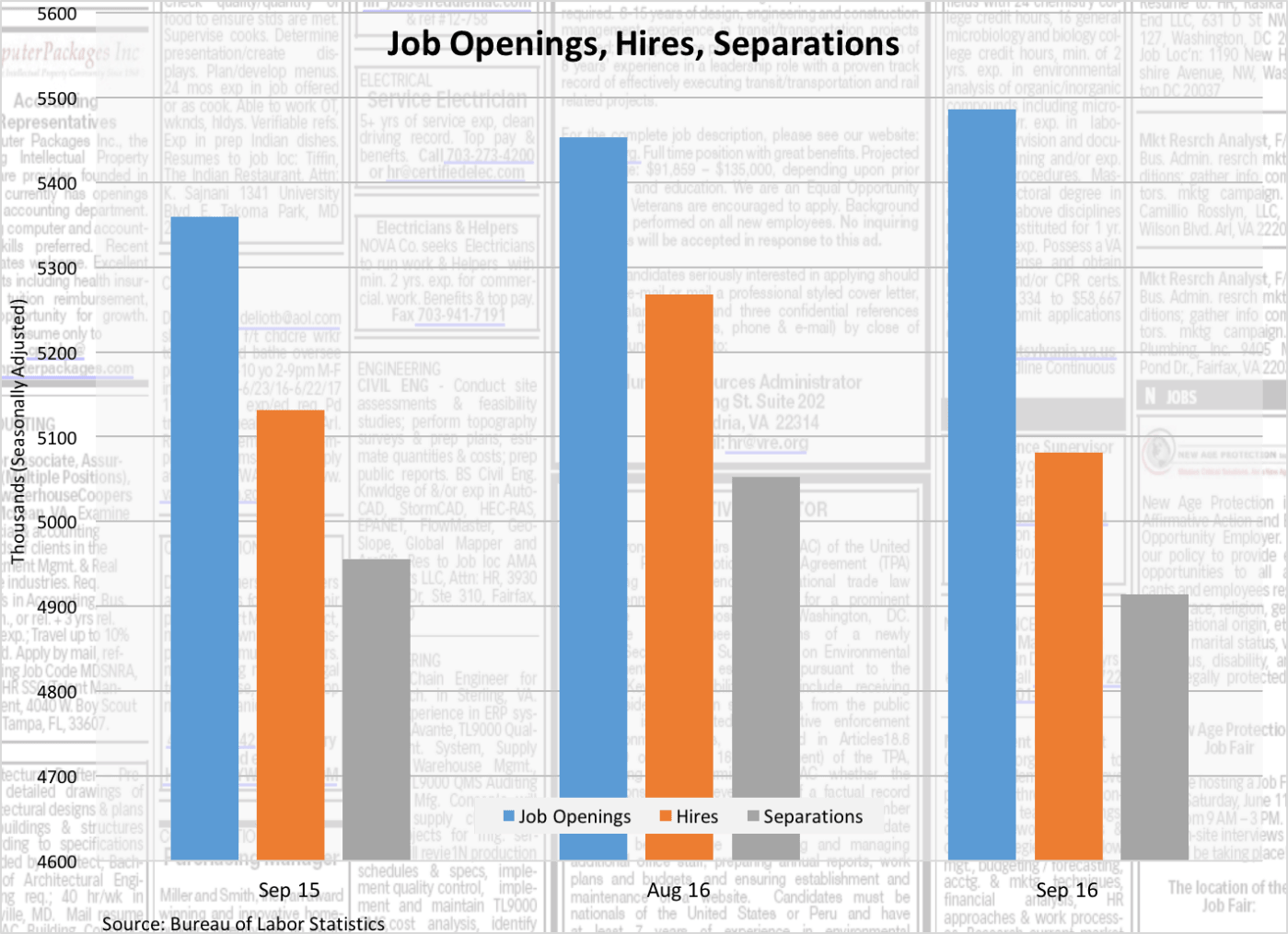

The number of job openings grew slightly while hiring slowed in September. The Bureau of Labor Statistics estimates that there were a seasonally adjusted 5.486 million job openings at the end of September. This was up 33,000 from August and 2.4% from a year earlier. The year-to-year growth rate in private sector job openings was slightly slower—the 4.987 million private sector job openings at the end of September represented a 2.2% gain from September 2015. Industries with the largest year-to-year gains in job gains were construction (+112.5%), manufacturing (+7.1%), transportation/warehousing (+6.5%), and retail (+2.1%). 5.081 million people were hired during September, off 187,000 from the prior month and down 0.9% from September 2015’s hiring pace. The largest positive 12-month comparables in hiring were in the government (+12.3%), transportation/warehousing (+4.4%), retail (+3.6%), wholesale trade (+3.0%), and professional/business services (+1.8%). Also falling were separations, dropping by 138,000 to 4.914 million. This was 0.8% below the year ago pace of separations. 3.270 million people voluntarily departed their jobs during September, down 581,000 from August but still 11.6% ahead of the September 2015 rate. Layoffs remained soft–at 1.610 million, layoffs declined 281,000 from August 2016 and was 21.7% below the year ago pace.

The number of job openings grew slightly while hiring slowed in September. The Bureau of Labor Statistics estimates that there were a seasonally adjusted 5.486 million job openings at the end of September. This was up 33,000 from August and 2.4% from a year earlier. The year-to-year growth rate in private sector job openings was slightly slower—the 4.987 million private sector job openings at the end of September represented a 2.2% gain from September 2015. Industries with the largest year-to-year gains in job gains were construction (+112.5%), manufacturing (+7.1%), transportation/warehousing (+6.5%), and retail (+2.1%). 5.081 million people were hired during September, off 187,000 from the prior month and down 0.9% from September 2015’s hiring pace. The largest positive 12-month comparables in hiring were in the government (+12.3%), transportation/warehousing (+4.4%), retail (+3.6%), wholesale trade (+3.0%), and professional/business services (+1.8%). Also falling were separations, dropping by 138,000 to 4.914 million. This was 0.8% below the year ago pace of separations. 3.270 million people voluntarily departed their jobs during September, down 581,000 from August but still 11.6% ahead of the September 2015 rate. Layoffs remained soft–at 1.610 million, layoffs declined 281,000 from August 2016 and was 21.7% below the year ago pace.

Wholesalers’ inventories largely held steady in September. Merchant wholesale inventories inched up 1/10th of a percent to a seasonally adjusted $590.2 billion. This was 0.1% below year ago levels for the Census Bureau measure. Inventories of durable goods contracted 0.4% during the month to $354.9 billion (-1.9% vs. September 2015), with inventory declines greater than 1.0% for metals, computer equipment, machinery, and automobiles. Nondurable goods inventories expanded 0.9% during the month to $235.3 billion (+2.7% vs. September 2015), reflecting sizable gains for petroleum (+3.8%), drugs (+3.3%), and paper (+0.8%). The inventory-to-sales (I/S) was at 1.33 in September, matching the ratios from both August 2016 and September 2015. The I/S ratio for durable goods slipped by a basis point to 1.66 while that for nondurable goods added a basis point to 1.02.

Wholesalers’ inventories largely held steady in September. Merchant wholesale inventories inched up 1/10th of a percent to a seasonally adjusted $590.2 billion. This was 0.1% below year ago levels for the Census Bureau measure. Inventories of durable goods contracted 0.4% during the month to $354.9 billion (-1.9% vs. September 2015), with inventory declines greater than 1.0% for metals, computer equipment, machinery, and automobiles. Nondurable goods inventories expanded 0.9% during the month to $235.3 billion (+2.7% vs. September 2015), reflecting sizable gains for petroleum (+3.8%), drugs (+3.3%), and paper (+0.8%). The inventory-to-sales (I/S) was at 1.33 in September, matching the ratios from both August 2016 and September 2015. The I/S ratio for durable goods slipped by a basis point to 1.66 while that for nondurable goods added a basis point to 1.02.

Small business owner sentiment edged up to its highest point in a year during October. The Small Business Optimism Index from the National Federation of Independent Business added 8/10ths of a point to a seasonally adjusted reading of 94.9. This was the measure’s best reading since October 2015 when it was at 96.0. The gain occurred even though only 5 of the index’s 10 components improved during the month, led by a big 9-point increase in the measure tracking respondents’ plans to increase inventories. Also improving from their September readings were index components for current job openings (up 4 points), current inventories (up 3 points), whether it is a good time to expand (up 2 points), and expected credit conditions (up a point). Falling sharply was the expected economic conditions index (down 7 points), with declines also seen for indices tracking expected real sales (down 3 points) and earning trends (down a point). The press release, published on election day, said that business owners “need predictability…that the political climate creates the opposite.”

Small business owner sentiment edged up to its highest point in a year during October. The Small Business Optimism Index from the National Federation of Independent Business added 8/10ths of a point to a seasonally adjusted reading of 94.9. This was the measure’s best reading since October 2015 when it was at 96.0. The gain occurred even though only 5 of the index’s 10 components improved during the month, led by a big 9-point increase in the measure tracking respondents’ plans to increase inventories. Also improving from their September readings were index components for current job openings (up 4 points), current inventories (up 3 points), whether it is a good time to expand (up 2 points), and expected credit conditions (up a point). Falling sharply was the expected economic conditions index (down 7 points), with declines also seen for indices tracking expected real sales (down 3 points) and earning trends (down a point). The press release, published on election day, said that business owners “need predictability…that the political climate creates the opposite.”

Consumer credit balances grew at a slower pace in September. The Federal Reserve places the value of outstanding non-real estate backed consumer loans at a seasonally adjusted $3.707 trillion, a gain of $19.3 billion from August and 6.0% from a year earlier. Non-revolving consumer credit balances—e.g., car loans, college loans—increased by $15.1 billion to $2.728 trillion (+6.0% vs. September 2015). Outstanding revolving consumer credit balances (including credit cards) expanded by $4.2 billion during September to $978.815 billion. (By comparison, revolving credit balanced increased $5.6 billion during August.) Revolving credit balances have grown 5.9% over the past year.

Consumer credit balances grew at a slower pace in September. The Federal Reserve places the value of outstanding non-real estate backed consumer loans at a seasonally adjusted $3.707 trillion, a gain of $19.3 billion from August and 6.0% from a year earlier. Non-revolving consumer credit balances—e.g., car loans, college loans—increased by $15.1 billion to $2.728 trillion (+6.0% vs. September 2015). Outstanding revolving consumer credit balances (including credit cards) expanded by $4.2 billion during September to $978.815 billion. (By comparison, revolving credit balanced increased $5.6 billion during August.) Revolving credit balances have grown 5.9% over the past year.

Banks report maintaining current lending standards to their commercial customers. According to survey data collected by the Federal Reserve and published in its latest edition of the Senior Loan Officer Opinion Survey on Bank Lending Practices, domestic banks kept their lending standards to both large/medium sized companies and to small firms “unchanged.” Some banks reported increasing the size of credit lines, shrinking the size of spreads between the cost of borrowed funds and their lending rates, and less frequent use of interest rate floors. At the same time, a small percentage of banks reported weaker demand for commercial loans from large/medium sized companies, but a “modest fraction” of banks reported greater interest in lines of credit from their commercial customers.

Banks report maintaining current lending standards to their commercial customers. According to survey data collected by the Federal Reserve and published in its latest edition of the Senior Loan Officer Opinion Survey on Bank Lending Practices, domestic banks kept their lending standards to both large/medium sized companies and to small firms “unchanged.” Some banks reported increasing the size of credit lines, shrinking the size of spreads between the cost of borrowed funds and their lending rates, and less frequent use of interest rate floors. At the same time, a small percentage of banks reported weaker demand for commercial loans from large/medium sized companies, but a “modest fraction” of banks reported greater interest in lines of credit from their commercial customers.

Other data released over the past week that you might find of interest:

– Jobless Claims (week ending November 5, 2016, First-Time Claims, seasonally adjusted): 254,000 (-11,000 vs. previous week; -22,000 vs. the same week a year earlier). 4-week moving average: 259,750 (-4.2% vs. the same week a year earlier).

– University of Michigan Index of Consumer Sentiment (November 2016-preliminary, Index (1966Q1=100, seasonally adjusted): 91.6 (vs. October 2016: 87.2, vs. November 2015: 91.3)

– Federal Government Budget (October 2016, Surplus/Deficit): -$44.2 billion (vs. October 2015: -$136.6 billion).

The opinions expressed here are not necessarily those of Kevin’s current and previous employers. No endorsements are implied.