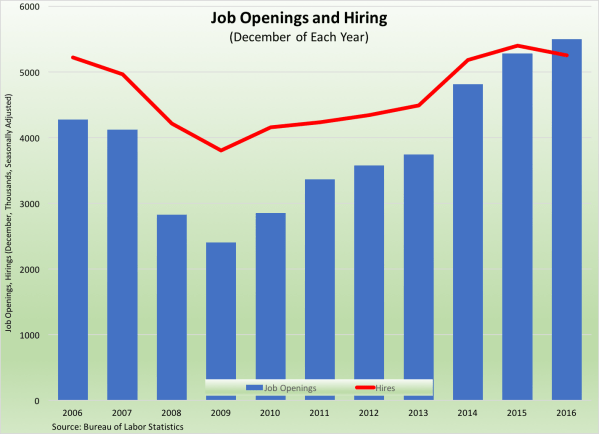

Data released last week finds the labor market held firm, but not necessarily improved, during the final days of 2016.

Job Openings Hold Steady, Trade Deficit Narrows: What We Learned During the Week of February 6 – 10

What We Learned About the U.S. Economy Last Week

Weekly Economic Update: A brief, non-technical review of the previous week's U.S. economic data releases by Kevin A. Roth, PhD

Data released last week finds the labor market held firm, but not necessarily improved, during the final days of 2016.