The labor market rebounded in June with accelerated hiring in health/social assistance and leisure/hospitality. Here are the five things we learned from U.S. economic data released during the week ending July 7.

Employers picked up hiring activity during June. The Bureau of Labor Statistics indicates nonfarm payrolls expanded during June by a seasonally adjusted 222,000, the best month for job creation since February. Further, the BLS upwardly revised its April and May employment estimates by a combined 47,000 jobs to +207,000 and +152,000, respectively. Private sector payrolls grew during June by 187,000 while government employers added 35,000 jobs. Private sector industries enjoying the largest payroll gains during the month were health care/social assistance (+59,100), leisure/hospitality (+36,000), professional/business services (+35,000), financial activities (+17,000), and construction (+16,000). Retailers added 8,100 workers following declines in April and May. The average work week grew by 1/10th of an hour to 34.5 hours (June 2016: 34.4 hours) with average weekly earnings up 2.8 percent from a year earlier to $905.63.

Employers picked up hiring activity during June. The Bureau of Labor Statistics indicates nonfarm payrolls expanded during June by a seasonally adjusted 222,000, the best month for job creation since February. Further, the BLS upwardly revised its April and May employment estimates by a combined 47,000 jobs to +207,000 and +152,000, respectively. Private sector payrolls grew during June by 187,000 while government employers added 35,000 jobs. Private sector industries enjoying the largest payroll gains during the month were health care/social assistance (+59,100), leisure/hospitality (+36,000), professional/business services (+35,000), financial activities (+17,000), and construction (+16,000). Retailers added 8,100 workers following declines in April and May. The average work week grew by 1/10th of an hour to 34.5 hours (June 2016: 34.4 hours) with average weekly earnings up 2.8 percent from a year earlier to $905.63.

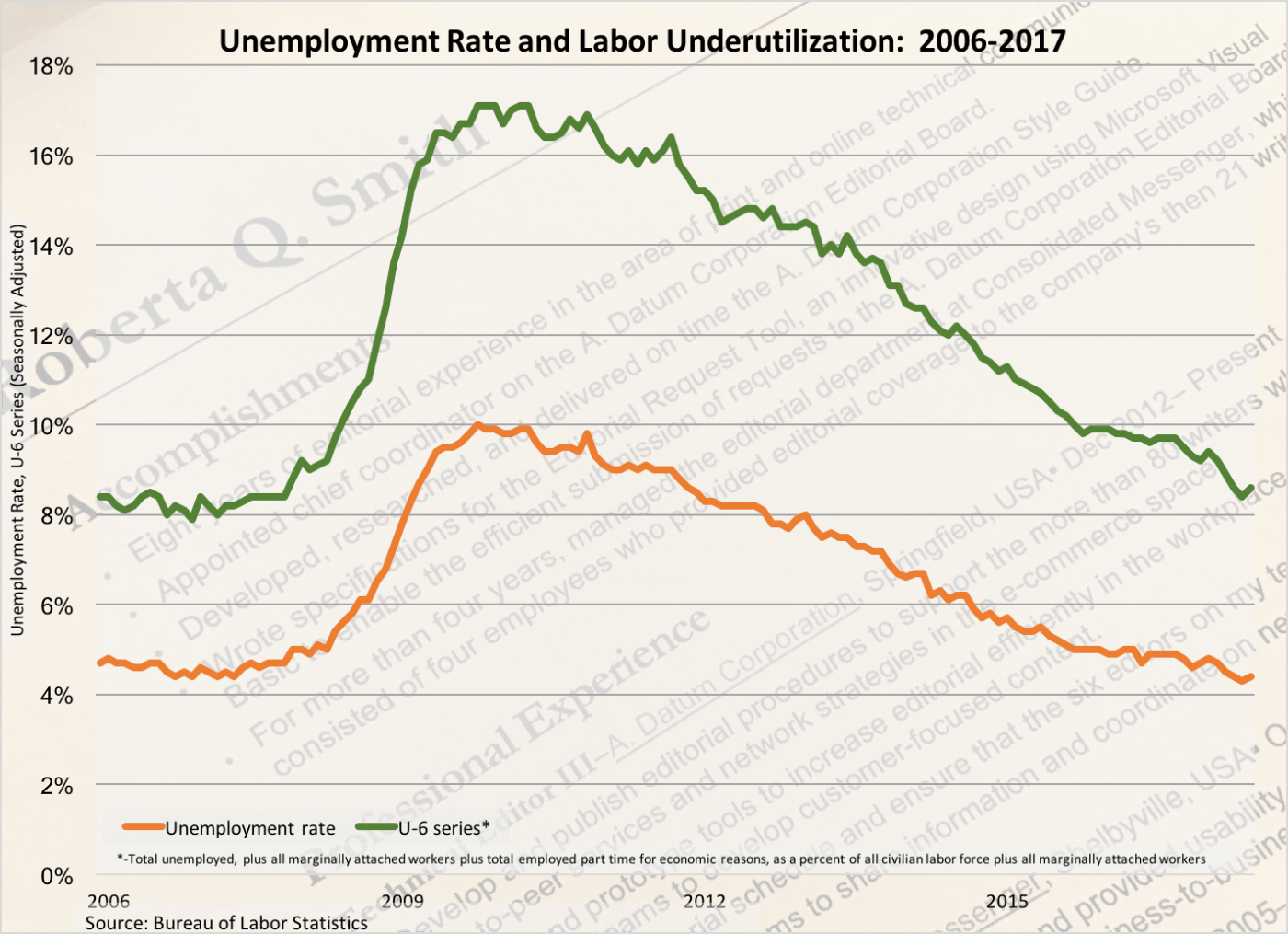

Based on a separate survey of households, the unemployment rate edged up by 1/10th of a percentage point to 4.4 percent. This was a half point below the year ago unemployment rate of 4.9 percent, leaving it near its post-recession low point. 361,000 people entered the labor force during the month, resulting in a 1/10th of a percentage point gain in the labor force participation rate to 62.8 percent. The median length of unemployment fell by 8/10ths of a week to 9.6 weeks (June 2016: 10.2 weeks). While the number of part-time workers seeking a full-time opportunity (“involuntary” part-time workers) increased by 107,000 during June, it was still 8.5 percent below the count of a year earlier. Finally, the broadest measure of labor underutilization (the “U6” series) increased 2/10ths of a percentage point to 8.6 percent, a full percentage point below the measure’s year-ago reading.

The trade deficit narrowed during May. The Census Bureau and Bureau of Economic Analysis report exports grew by $0.9 billion during the month to $192.0 billion (+5.4 percent vs. May 2016) while imports narrowed by $0.2 billion to $238.5 billion (+6.6 percent vs. May 2016). This left the trade deficit at $46.5 billion, $1.1 billion smaller than that of April but up 12.0 percent over the past year. The goods deficit contracted by $0.9 billion to -$67.5 billion while the goods surplus widened by $0.2 billion to +$21.0 billion. Exports grew during the month for automotive vehicles (+$0.6 billion) and cell phones/other household goods (+$0.5 billion) but slowed for soybeans (-$0.6 billion). Imports fell for consumer goods (-$1.5 billion, including -$0.9 billion for cell phones), automotive vehicles (-$0.7 billion), but grew by $1.3 billion for capital goods. The trade deficit for the first five months of 2017 was 13.1 percent larger than that of 2016, the result of exports growing 6.0 percent and imports expanding 7.3 percent.

The trade deficit narrowed during May. The Census Bureau and Bureau of Economic Analysis report exports grew by $0.9 billion during the month to $192.0 billion (+5.4 percent vs. May 2016) while imports narrowed by $0.2 billion to $238.5 billion (+6.6 percent vs. May 2016). This left the trade deficit at $46.5 billion, $1.1 billion smaller than that of April but up 12.0 percent over the past year. The goods deficit contracted by $0.9 billion to -$67.5 billion while the goods surplus widened by $0.2 billion to +$21.0 billion. Exports grew during the month for automotive vehicles (+$0.6 billion) and cell phones/other household goods (+$0.5 billion) but slowed for soybeans (-$0.6 billion). Imports fell for consumer goods (-$1.5 billion, including -$0.9 billion for cell phones), automotive vehicles (-$0.7 billion), but grew by $1.3 billion for capital goods. The trade deficit for the first five months of 2017 was 13.1 percent larger than that of 2016, the result of exports growing 6.0 percent and imports expanding 7.3 percent.

The decline in new factory orders accelerated in May. The Census Bureau reports that new orders for manufactured goods fell 0.8 percent during the month following a 0.3 percent drop in April. The resulting seasonally adjusted value of new orders of $464.9 billion was up 4.2 percent from a year earlier. Both durable and nondurable goods orders slowed by a similar 0.8 percent rate while those of nondefense, nonaircraft capital goods (a measure of business investment) edged up 0.2 percent. Shipments grew for the fifth time in six months with a 0.1 percent increase to $471.5 billion. Durable goods shipments rose 1.0 percent while nondurable goods shipments slowed 0.8 percent. Unfilled order shrank 0.2 percent to $1.120 trillion while inventories contracted 0.1 percent to $648.9 billion.

The decline in new factory orders accelerated in May. The Census Bureau reports that new orders for manufactured goods fell 0.8 percent during the month following a 0.3 percent drop in April. The resulting seasonally adjusted value of new orders of $464.9 billion was up 4.2 percent from a year earlier. Both durable and nondurable goods orders slowed by a similar 0.8 percent rate while those of nondefense, nonaircraft capital goods (a measure of business investment) edged up 0.2 percent. Shipments grew for the fifth time in six months with a 0.1 percent increase to $471.5 billion. Durable goods shipments rose 1.0 percent while nondurable goods shipments slowed 0.8 percent. Unfilled order shrank 0.2 percent to $1.120 trillion while inventories contracted 0.1 percent to $648.9 billion.

Purchasing managers report that both manufacturing and service sector business activity grew during June. The Purchasing Managers Index (PMI) from the Institute for Supply Management gained 2.9 points during June to a seasonally adjusted 57.8. This was the 10th straight month in which the measure was above a reading of 50.0, indicative of an expanding manufacturing sector. Four of five PMI components improved during the month: production (up 5.3 points to 62.4), new orders (up 4.0 points to 63.5), supplier deliveries (up 3.7 points to 57.2), and employment (up 3.7 points to 57.2). The index tracking inventories shed 2.5 points to a contractionary reading of 49.0. Fifteen of 18 tracked manufacturing industry segments expanded during the month, led by furniture, nonmetallic mineral productions, and paper products. The press release indicated that survey respondent comments noted “expanding business” but that “supplier deliveries and inventories [were] struggling to keep up with the production pace.”

Purchasing managers report that both manufacturing and service sector business activity grew during June. The Purchasing Managers Index (PMI) from the Institute for Supply Management gained 2.9 points during June to a seasonally adjusted 57.8. This was the 10th straight month in which the measure was above a reading of 50.0, indicative of an expanding manufacturing sector. Four of five PMI components improved during the month: production (up 5.3 points to 62.4), new orders (up 4.0 points to 63.5), supplier deliveries (up 3.7 points to 57.2), and employment (up 3.7 points to 57.2). The index tracking inventories shed 2.5 points to a contractionary reading of 49.0. Fifteen of 18 tracked manufacturing industry segments expanded during the month, led by furniture, nonmetallic mineral productions, and paper products. The press release indicated that survey respondent comments noted “expanding business” but that “supplier deliveries and inventories [were] struggling to keep up with the production pace.”

The ISM’s measure of nonmanufacturing economic activity added a half point during June to 57.4, the 90th consecutive month in which the NMI was above a reading of 50.0. Three of four index components improved from their June marks: new orders (up 2.8 points to 60.5), supplier deliveries (up a full point to 52.5), and business activity/production (up 1/10th of a point to 60.8). The employment index shed two full points to 57.8. Sixteen of 18 tracked service sector industries expanded during June, led by agriculture, wholesale trade, management of companies/support. The press release said that the “majority of respondents’ comments are positive about business conditions and the overall economy.”

Vehicle sales continued to slacken in June. Per automaker sales data compiled by Autodata, the seasonally adjusted annualized rate of vehicle sales was below 17 million units for a fourth straight month. The annualized sales rate of 16.50 million vehicles was down 1.0 percent from May and 1.8 percent from a year earlier. Car sales continued to slump, dropping 4.7 percent during the month and 13.2 percent from June 2016 to an annualized rate of 5.91 million vehicles. Light truck/SUV sales inched up 1.3 percent during June to an annualized rate of 10.60 million vehicles. This was 5.8 percent above light truck/SUV sales of a year earlier

Vehicle sales continued to slacken in June. Per automaker sales data compiled by Autodata, the seasonally adjusted annualized rate of vehicle sales was below 17 million units for a fourth straight month. The annualized sales rate of 16.50 million vehicles was down 1.0 percent from May and 1.8 percent from a year earlier. Car sales continued to slump, dropping 4.7 percent during the month and 13.2 percent from June 2016 to an annualized rate of 5.91 million vehicles. Light truck/SUV sales inched up 1.3 percent during June to an annualized rate of 10.60 million vehicles. This was 5.8 percent above light truck/SUV sales of a year earlier

Other U.S. economic data released over the past week:

– Jobless Claims (week ending July 1, 2017, First-Time Claims, seasonally adjusted): 248,000 +4,000 vs. previous week; -11,000 vs. the same week a year earlier). 4-week moving average: 243,000 (-8.4% vs. the same week a year earlier).

– Construction Spending (May 2017, Value of Construction Put in Place, seasonally adjusted annual rate): $1.230 trillion (unchanged vs. April 2017, +4.5% vs. May 2016).

– FOMC minutes

The opinions expressed here are not necessarily those of Kevin’s current and previous employers. No endorsements are implied.