Home sales hit a ten-year high in March and housing starts remained solid. But the manufacturing sector ends its recent winning streak. Here are the 5 things we learned from U.S. economic data released during the week ending April 21.

Existing home sales hit another post-recession high in March. The National Association of Realtors reports that existing home sales jumped 4.4 percent during the month to a seasonally adjusted annualized rate (SAAR) of 5.710 million homes. This was up 5.9 percent from a year earlier and represented the best month for sales of previously owned homes since February 2007. Sales grew in three of four Census regions: Northeast (+10.1 percent), Midwest (+9.2 percent), and South (+3.4 percent). Sales slipped 1.6 percent in the West. All four Census regions enjoyed positive 12-month sales comparables. Even though inventories of unsold homes grew 5.8 percent during the month, the 1.830 million homes available for sale at the end of March was a 6.6 percent drop from a year earlier and represented a very tight 3.8 month supply. As a result, the median sales price for existing homes has risen 6.8 percent over the past year to $236,400. The press release described the spring home buying season as “promising,” but noted that “finding available properties to buy continues to be a strenuous task for many buyers.”

Existing home sales hit another post-recession high in March. The National Association of Realtors reports that existing home sales jumped 4.4 percent during the month to a seasonally adjusted annualized rate (SAAR) of 5.710 million homes. This was up 5.9 percent from a year earlier and represented the best month for sales of previously owned homes since February 2007. Sales grew in three of four Census regions: Northeast (+10.1 percent), Midwest (+9.2 percent), and South (+3.4 percent). Sales slipped 1.6 percent in the West. All four Census regions enjoyed positive 12-month sales comparables. Even though inventories of unsold homes grew 5.8 percent during the month, the 1.830 million homes available for sale at the end of March was a 6.6 percent drop from a year earlier and represented a very tight 3.8 month supply. As a result, the median sales price for existing homes has risen 6.8 percent over the past year to $236,400. The press release described the spring home buying season as “promising,” but noted that “finding available properties to buy continues to be a strenuous task for many buyers.”

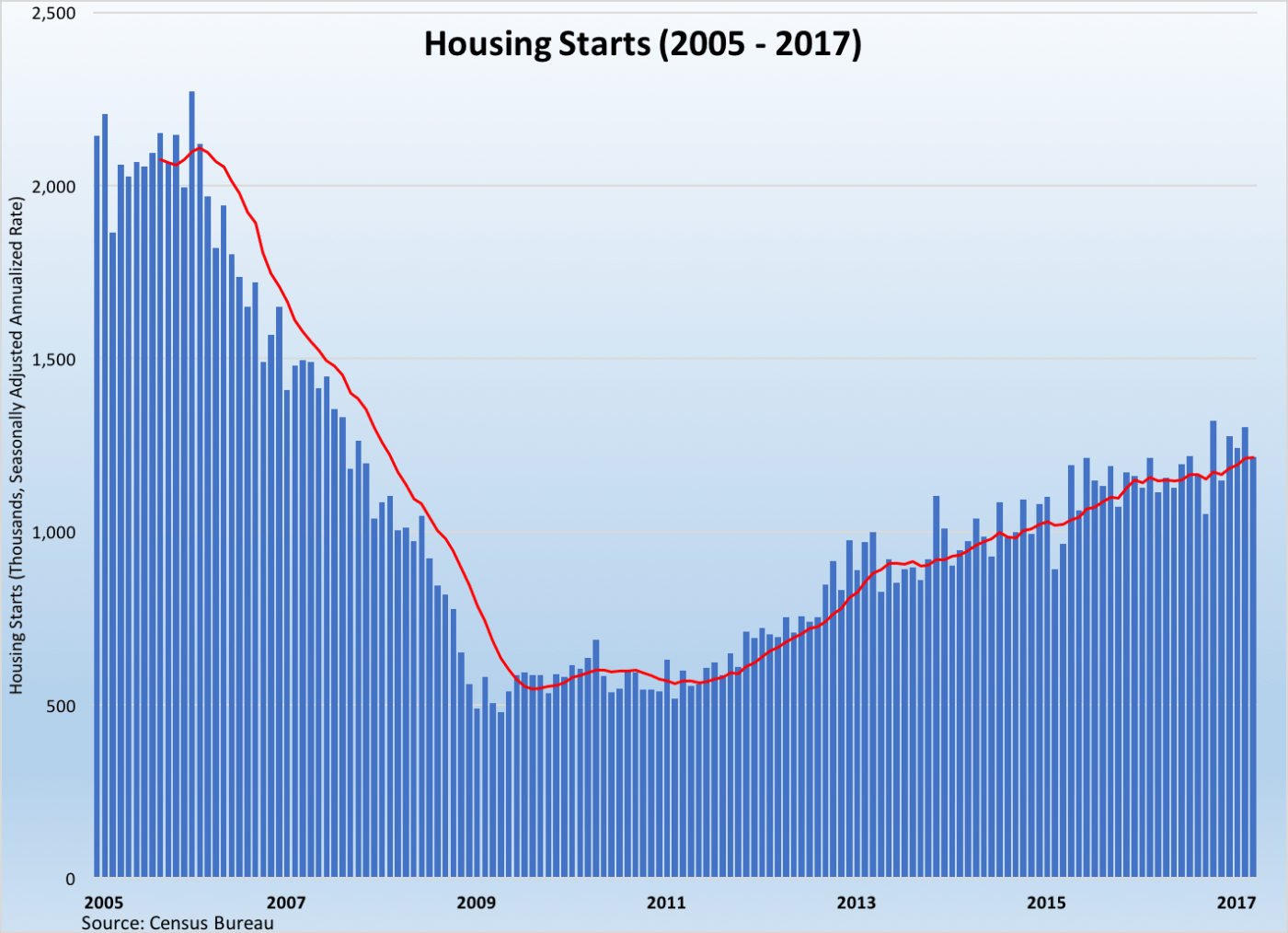

Housing starts slip but remained near post-recession highs in March. Per the Census Bureau, housing starts were at a seasonally adjusted annualized rate (SAAR) of 1.215 million units, down 6.8 percent for the month but still 9.2 percent its March 2016 pace. (Note that while housing starts were near their post-recession high, they remained well below the peak values seen during the early and middle part of the last decade.) While both the month-to-month and year-to-year comparables were equivalent for both single-family and multi-family properties, they did differ by region. Versus February, starts grew 12.9 percent in the Northeast but dropped 16.2 percent in the Midwest, 16.0 percent in the West, and 3.2 percent in the South. Starts have grown over the past year in the South (+19.4 percent) and West (+9.2 percent) while they have fallen in the Northeast (-14.9 percent) and Midwest (-2.5 percent). Looking towards the future, the SAAR of issued building permits grew 3.6 percent during March to 1.26 million permits (+17.0 percent). Permit issuance was up sharply in all four Census regions: Northeast (+26.1 percent), West (+24.5 percent), South (+14.6 percent), and Midwest (+4.9 percent). The annualized rate of housing completions grew 3.2 percent during the month to 1.168 million units. This was a healthy 13.4 percent above the March 2016 pace of completions.

Housing starts slip but remained near post-recession highs in March. Per the Census Bureau, housing starts were at a seasonally adjusted annualized rate (SAAR) of 1.215 million units, down 6.8 percent for the month but still 9.2 percent its March 2016 pace. (Note that while housing starts were near their post-recession high, they remained well below the peak values seen during the early and middle part of the last decade.) While both the month-to-month and year-to-year comparables were equivalent for both single-family and multi-family properties, they did differ by region. Versus February, starts grew 12.9 percent in the Northeast but dropped 16.2 percent in the Midwest, 16.0 percent in the West, and 3.2 percent in the South. Starts have grown over the past year in the South (+19.4 percent) and West (+9.2 percent) while they have fallen in the Northeast (-14.9 percent) and Midwest (-2.5 percent). Looking towards the future, the SAAR of issued building permits grew 3.6 percent during March to 1.26 million permits (+17.0 percent). Permit issuance was up sharply in all four Census regions: Northeast (+26.1 percent), West (+24.5 percent), South (+14.6 percent), and Midwest (+4.9 percent). The annualized rate of housing completions grew 3.2 percent during the month to 1.168 million units. This was a healthy 13.4 percent above the March 2016 pace of completions.

Industrial production rose during March, but manufacturing output did not. The Federal Reserve reports that industrial production grew 0.5 percent during March, following a tepid 0.1 percent increase during February and a 0.3 percent decline during January. The increase was largely the result of an 8.6 percent surge in output at utilities as weather conditions returned to their seasonal norms after an abnormally warm winter had suppressed demand for heating. Mining output edged up 0.1 percent during the month. On the flip side, manufacturing production fell 0.4 percent during March and was only 0.8 percent above its year ago level. This was the first monthly decline in manufacturing output since last August. The production of durable manufactured goods dropped 0.8 percent with all major categories of durable products reporting output declines (except for computers/electronics). Falling by at least one percent was the output of automobiles, electrical equipment/appliances, and primary metals. Production of nondurables eked out a 0.2 percent gain, with petroleum/coal products seeing the largest gain in output. Capacity utilization increased 4/10ths of a percentage point to 76.1 percent, but the same measure for the manufacturing sector saw factory utilization declining by 3/10ths of a percentage point to 75.7 percent.

Industrial production rose during March, but manufacturing output did not. The Federal Reserve reports that industrial production grew 0.5 percent during March, following a tepid 0.1 percent increase during February and a 0.3 percent decline during January. The increase was largely the result of an 8.6 percent surge in output at utilities as weather conditions returned to their seasonal norms after an abnormally warm winter had suppressed demand for heating. Mining output edged up 0.1 percent during the month. On the flip side, manufacturing production fell 0.4 percent during March and was only 0.8 percent above its year ago level. This was the first monthly decline in manufacturing output since last August. The production of durable manufactured goods dropped 0.8 percent with all major categories of durable products reporting output declines (except for computers/electronics). Falling by at least one percent was the output of automobiles, electrical equipment/appliances, and primary metals. Production of nondurables eked out a 0.2 percent gain, with petroleum/coal products seeing the largest gain in output. Capacity utilization increased 4/10ths of a percentage point to 76.1 percent, but the same measure for the manufacturing sector saw factory utilization declining by 3/10ths of a percentage point to 75.7 percent.

Forward-looking data suggest continued economic growth for the remainder of this year. The Conference Board’s Leading Economic Indicators added a half point during March to a hit a seasonally adjusted 126.7 (2010=100). This left the measure 3.5 percent above where it was a year earlier. Eight of the leading index’s components improved during the month, led by the interest rate spread, purchasing managers’ report on new orders, and consumers’ expectations for future business conditions. The coincident index added 2/10ths of a point 114.9 (+2.0 percent vs. March 2016) with all 4 of the measure’s components making a positive contribution to the index (including, industrial production and personal income). The lagging index held firm at 123.6 during the month, which left the measure 2.3 percent above where it was a year ago. Three of the seven components of the lagging index made positive contributions, led by banks’ prime rate for loans. The press release stated the results suggest continued economic growth in 2017, “with perhaps an acceleration later in the year if consumer spending and investment pick up.”

Forward-looking data suggest continued economic growth for the remainder of this year. The Conference Board’s Leading Economic Indicators added a half point during March to a hit a seasonally adjusted 126.7 (2010=100). This left the measure 3.5 percent above where it was a year earlier. Eight of the leading index’s components improved during the month, led by the interest rate spread, purchasing managers’ report on new orders, and consumers’ expectations for future business conditions. The coincident index added 2/10ths of a point 114.9 (+2.0 percent vs. March 2016) with all 4 of the measure’s components making a positive contribution to the index (including, industrial production and personal income). The lagging index held firm at 123.6 during the month, which left the measure 2.3 percent above where it was a year ago. Three of the seven components of the lagging index made positive contributions, led by banks’ prime rate for loans. The press release stated the results suggest continued economic growth in 2017, “with perhaps an acceleration later in the year if consumer spending and investment pick up.”

A closer look at March employment data finds payrolls were unchanged in most states. The Bureau of Labor Statistics’ Regional and State Employment report indicates that there were statistically significant increases in nonfarm payrolls during the month in three states: Washington state (+10,000). Tennessee (+8,600), and Maine (+3,000). Payrolls declined in four other states: New Jersey (-17,500), Pennsylvania (-16,100), Missouri (-13,400), and Louisiana (-8,500). Payrolls did not significantly change in the other 43 states and in the District of Columbia during the month. Even with the relative stagnation during March, nonfarm payrolls have expanded in 27 states over the past year, with the largest percentage gains occurring in Utah, Florida, Georgia, and Nevada. Only two states—Alaska and Wyoming—suffered year-to-year payroll declines.

A closer look at March employment data finds payrolls were unchanged in most states. The Bureau of Labor Statistics’ Regional and State Employment report indicates that there were statistically significant increases in nonfarm payrolls during the month in three states: Washington state (+10,000). Tennessee (+8,600), and Maine (+3,000). Payrolls declined in four other states: New Jersey (-17,500), Pennsylvania (-16,100), Missouri (-13,400), and Louisiana (-8,500). Payrolls did not significantly change in the other 43 states and in the District of Columbia during the month. Even with the relative stagnation during March, nonfarm payrolls have expanded in 27 states over the past year, with the largest percentage gains occurring in Utah, Florida, Georgia, and Nevada. Only two states—Alaska and Wyoming—suffered year-to-year payroll declines.

Other U.S. economic data released over the past week:

– Jobless Claims (week ending April 15, 2017, First-Time Claims, seasonally adjusted): 244,000 (+10,000 vs. previous week; -13,000 vs. the same week a year earlier). 4-week moving average: 247,250 (-8.4% vs. the same week a year earlier).

– NAHB Housing Market Index (April 2017, Index (>50 = “Good” Housing Market Conditions), seasonally adjusted): 68 (vs. March 2017: 71, vs. April 2016: 58).

– Bankruptcy Filings (12-month period through March 31, 2017): 794,492 (-4.7 percent versus 12-month period through March 31, 2016). Business bankruptcy filings: 770,901 (-4.7 percent vs. March 31, 2016), Nonbusiness bankruptcy filings: 23,591 (-4.9 percent versus March 31, 2016).

– Treasury International Capital Flows (February 2017, Foreign Purchases of Domestic U.S. Securities, not seasonally adjusted): +$35.9 billion (vs. January 2017: +$14.8 billion., vs. February 2016; +$26.9 billion).

– Beige Book

The opinions expressed here are not necessarily those of Kevin’s current and previous employers. No endorsements are implied.