The number of job openings hit another post-recession high in July. Yet, the same month was not so hot for the service sector. Here are the 5 things we learned from U.S. economic data released during the week ending September 9.

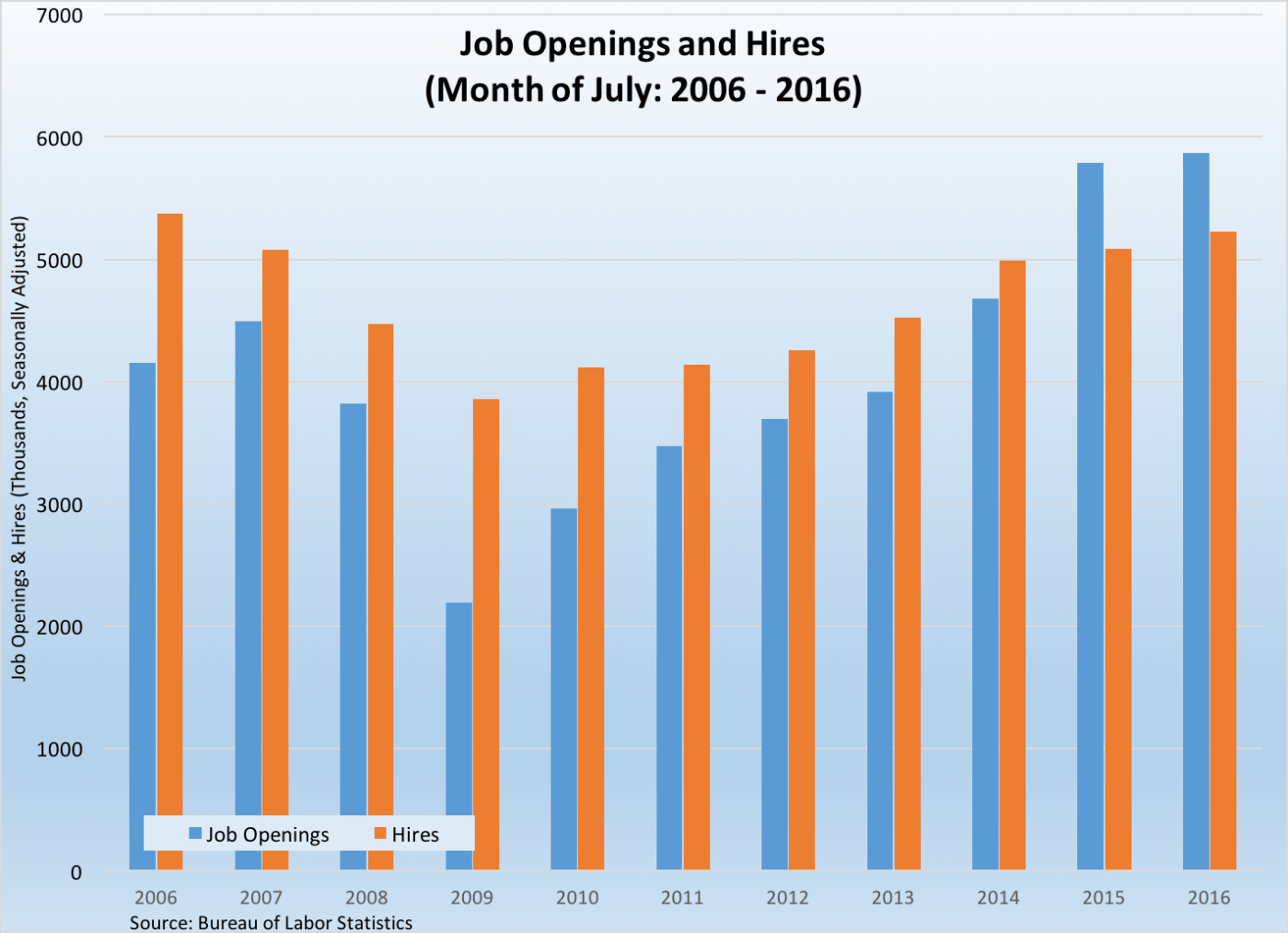

Employers posted more job openings during July but expanded payrolls at a slower pace. The Bureau of Labor Statistics reports that there were a seasonally adjusted 5.871 million job openings at the end of the month, up 228,000 from June, 1.4% above year ago levels, and the most in the 16+ year history of the data series. This included 5.358 million private sector job openings (+2.2% vs. July 2015), with positive 12-month comparables in construction (+41.7%), professional/business services (+12.9%), transportation/warehousing (+7.2%), retail (+3.8%), and manufacturing (+3.6%). The number of job openings was below year ago levels in mining/logging (-43.5%), wholesale trade (-21.4%), financial activities (-12.3%), and the government (-6.0%). The number of people hired during the month expanded by “only” 97,000 jobs to 5.227 million hires, 2.8% above year ago levels. Private sector hiring totaled 4.861 million, a 3.2% gain from July 2015. Industries with the largest year-to-year percentage gains in hiring were professional/business services (+13.7%), construction (+11.0%), leisure/hospitality (+10.4%), and manufacturing (+3.8%). Job separations were 3.0% above year ago levels at 4.937 million, with voluntary quits (+9.4%) higher and layoffs (-5.1%) below their July 2015 readings.

Employers posted more job openings during July but expanded payrolls at a slower pace. The Bureau of Labor Statistics reports that there were a seasonally adjusted 5.871 million job openings at the end of the month, up 228,000 from June, 1.4% above year ago levels, and the most in the 16+ year history of the data series. This included 5.358 million private sector job openings (+2.2% vs. July 2015), with positive 12-month comparables in construction (+41.7%), professional/business services (+12.9%), transportation/warehousing (+7.2%), retail (+3.8%), and manufacturing (+3.6%). The number of job openings was below year ago levels in mining/logging (-43.5%), wholesale trade (-21.4%), financial activities (-12.3%), and the government (-6.0%). The number of people hired during the month expanded by “only” 97,000 jobs to 5.227 million hires, 2.8% above year ago levels. Private sector hiring totaled 4.861 million, a 3.2% gain from July 2015. Industries with the largest year-to-year percentage gains in hiring were professional/business services (+13.7%), construction (+11.0%), leisure/hospitality (+10.4%), and manufacturing (+3.8%). Job separations were 3.0% above year ago levels at 4.937 million, with voluntary quits (+9.4%) higher and layoffs (-5.1%) below their July 2015 readings.

Service sector growth appreciably slowed in August. The headline index from the Institute for Supply Management’s Report on Business shed 4.1 points to a seasonally adjusted 51.4. While this was the 79th straight month in which the measure was above the expansionary/contractionary threshold of 50.0, it was its lowest reading since February 2010. 3 of 4 headline index components declined during the month (business activity, new orders, and employment) while the measure for supplier deliveries improved from its July mark. 11 of 18 tracked service sector industries expanded during the month, led by utilities, real estate, accommodation/food services, and finance/insurance. The press release notes that a “majority” of companies participating in the survey had reported a “slowing in the level of business.”

Service sector growth appreciably slowed in August. The headline index from the Institute for Supply Management’s Report on Business shed 4.1 points to a seasonally adjusted 51.4. While this was the 79th straight month in which the measure was above the expansionary/contractionary threshold of 50.0, it was its lowest reading since February 2010. 3 of 4 headline index components declined during the month (business activity, new orders, and employment) while the measure for supplier deliveries improved from its July mark. 11 of 18 tracked service sector industries expanded during the month, led by utilities, real estate, accommodation/food services, and finance/insurance. The press release notes that a “majority” of companies participating in the survey had reported a “slowing in the level of business.”

Consumers continued to take on additional debt in July, but the growth in credit card balances decelerated. Consumers had non-real estate backed outstanding credit balances of $3.661 trillion, up $17.7 billion for the month. The 6.0% increase in the Federal Reserve measure over the past year reflected a slightly smaller 12-month comparable in comparison to what we have seen over the past few years. Outstanding nonrevolving credit balances (e.g., auto and college loans) expanded by $14.9 billion during the month to $2.692 trillion (+6.0% vs. July 2015). Outstanding revolving credit balances (i.e., credit cards) edged up by only $2.8 billion (following gains of $9.2 billion and $4.6 billion during the 2 previous months) to $969.0 billion. This also was 6.0% ahead of July 2015 outstanding balances.

Consumers continued to take on additional debt in July, but the growth in credit card balances decelerated. Consumers had non-real estate backed outstanding credit balances of $3.661 trillion, up $17.7 billion for the month. The 6.0% increase in the Federal Reserve measure over the past year reflected a slightly smaller 12-month comparable in comparison to what we have seen over the past few years. Outstanding nonrevolving credit balances (e.g., auto and college loans) expanded by $14.9 billion during the month to $2.692 trillion (+6.0% vs. July 2015). Outstanding revolving credit balances (i.e., credit cards) edged up by only $2.8 billion (following gains of $9.2 billion and $4.6 billion during the 2 previous months) to $969.0 billion. This also was 6.0% ahead of July 2015 outstanding balances.

Consistent with the report above, layoff activity remained relatively light during the final days of summer. The Department of Labor reports that were 259,000 1st time claims made for unemployment insurance benefits on a seasonally adjusted basis during the week ending September 3rd. Weekly 1st time claims have been under 300,000 every week for more than year and a half. This was down 4,000 from the prior week and 16,000 below the count from the same week a year earlier. The 4-week moving average slipped by 1,750 to 261,250 claims (-5.5% below year ago levels). 2.055 million people were receiving some form of unemployment insurance benefits during the week ending August 20, a 4.6% drop from the year ago count.

Consistent with the report above, layoff activity remained relatively light during the final days of summer. The Department of Labor reports that were 259,000 1st time claims made for unemployment insurance benefits on a seasonally adjusted basis during the week ending September 3rd. Weekly 1st time claims have been under 300,000 every week for more than year and a half. This was down 4,000 from the prior week and 16,000 below the count from the same week a year earlier. The 4-week moving average slipped by 1,750 to 261,250 claims (-5.5% below year ago levels). 2.055 million people were receiving some form of unemployment insurance benefits during the week ending August 20, a 4.6% drop from the year ago count.

The latest Beige Book once again finds a moderate pace of economic expansion. The latest edition of the Federal Reserve’s compilation of anecdotal information and insights as collected by the 12 district banks characterizes economic activity as expanding “at a modest pace” during all of July and the first half of August. Further, most of the business contacts interviewed for the report “expect moderate economic growth” into the fall. Consumer spending was “little changed,” although spending on automobiles had slowed. Nonfinancial services “gained further momentum” while manufacturing “rose slightly.” Residential real estate “grew at a moderate pace,” although tight inventories were constraining sales activity in some markets. Labor market conditions were described as “tight” with “moderate” payrolls growth (although there were some “upward wage pressures.”) Nevertheless, price gains had “remained slight overall.”

The latest Beige Book once again finds a moderate pace of economic expansion. The latest edition of the Federal Reserve’s compilation of anecdotal information and insights as collected by the 12 district banks characterizes economic activity as expanding “at a modest pace” during all of July and the first half of August. Further, most of the business contacts interviewed for the report “expect moderate economic growth” into the fall. Consumer spending was “little changed,” although spending on automobiles had slowed. Nonfinancial services “gained further momentum” while manufacturing “rose slightly.” Residential real estate “grew at a moderate pace,” although tight inventories were constraining sales activity in some markets. Labor market conditions were described as “tight” with “moderate” payrolls growth (although there were some “upward wage pressures.”) Nevertheless, price gains had “remained slight overall.”

Other data released over the past week that you might find of interest:

– Wholesale Inventories (July 2016, seasonally adjusted): $591.3 billion (unchanged vs. June 2016, +0.5% vs. July 2015).

The opinions expressed here are not necessarily those of Kevin’s current and previous employers. No endorsements are implied.