The Federal Reserve does not act again (although it is still expecting to do so in 2016) while manufacturing takes another break. Here are the 5 things we learned from U.S. economic data released during the week ending June 17.

The Fed holds still again, but is forecasting 2 rate hikes in 2016…no, seriously. Following the unexpectedly weak May employment report, it was of little surprise that the Federal Open Market Committee decided to keep the fed funds target rate at between 0.25% and 0.50%. The policy statement released following last week’s FOMC meeting did note that economic growth “appears to have picked up,” but also said that job creation had “diminished.” Further inflation remained below the Fed’s 2 percent target rate with long-term expectations having “little changed, on balance, in recent months.” All voting FOMC members concurred with the decision to stay put, including Kansas City Fed President Esther George, who had been pushing for a rate hike at recent meetings.

The Fed holds still again, but is forecasting 2 rate hikes in 2016…no, seriously. Following the unexpectedly weak May employment report, it was of little surprise that the Federal Open Market Committee decided to keep the fed funds target rate at between 0.25% and 0.50%. The policy statement released following last week’s FOMC meeting did note that economic growth “appears to have picked up,” but also said that job creation had “diminished.” Further inflation remained below the Fed’s 2 percent target rate with long-term expectations having “little changed, on balance, in recent months.” All voting FOMC members concurred with the decision to stay put, including Kansas City Fed President Esther George, who had been pushing for a rate hike at recent meetings.

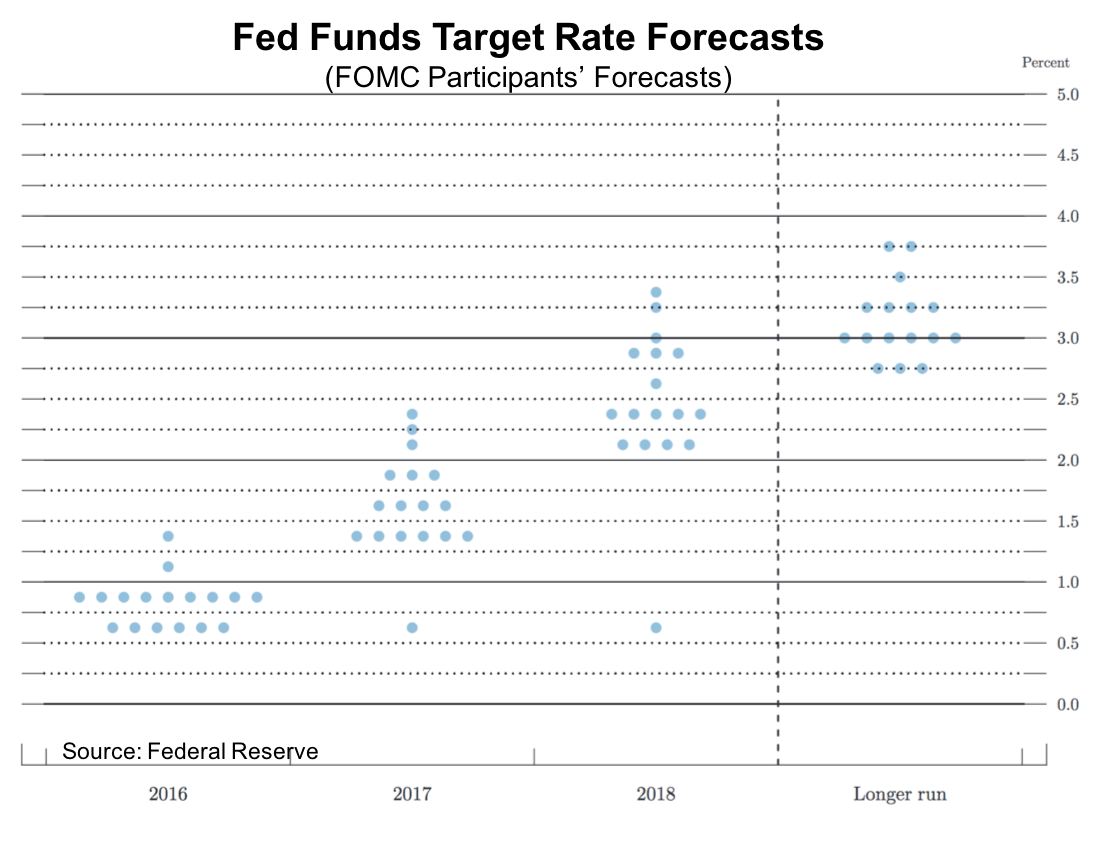

Accompanying the policy statement was the latest set of economic forecasts from FOMC participants. The median forecast for 2016 and 2017 GDP growth slipped to +2.0% for both years (from +2.2% and 2.1%, respectively, when the last set of forecasts released in March). While the unemployment rate for 2016 and 2017 held steady from the March forecasts of 4.7% and 4.6%, respectively, the forecast for core personal consumption expenditures (PCE) inflation edged up 1/10th of a percentage point to +1.7% and 1.8%, respectively. Meanwhile, the median forecast sees 2 quarter-point hikes in the fed funds target rate before this year ends, although 6 FOMC participants only anticipate a single rate hike by this December. The median forecast for the fed funds target rate at the end of 2017 is now at 1.625%, down from the March’s forecast of 1.875%. Further, the end of 2018 rate forecast of 2.375% is down from the 3.00% forecast reported in March.

A slowdown at auto plants weighs on manufacturing activity during May. The Federal Reserve estimates manufacturing activity slowed 0.4% during May, its 2nd decline in 3 months. Output of durable goods slowed 0.7%, hurt by a 4.2% drop in auto production and a declines greater than 1.0% for wood products and machinery. Manufacturing activity for nondurable goods was flat for the month as increased output of food/beverage products and paper outweighed drops for most other nondurable goods products. Manufacturing output was 0.2% below year ago levels. This data comes from the Fed’s Industrial Production report, which has overall factory output declining for the 3rd time in 4 months (-0.4%) and being down 1.4% from a year earlier. Mining output (e.g., oil, coal) eked out a 0.2% gain following 8 consecutive monthly declines that left the measure 11.5% below year ago levels. Output at utilities fell for the 3rd time in 4 months with a 1.0% drop. Factory utilization slowed by 4/10ths of a percentage point to 74.9%–the same measure for the manufacturing sector also shed 4/10ths of a percentage point to 74.8%.

A slowdown at auto plants weighs on manufacturing activity during May. The Federal Reserve estimates manufacturing activity slowed 0.4% during May, its 2nd decline in 3 months. Output of durable goods slowed 0.7%, hurt by a 4.2% drop in auto production and a declines greater than 1.0% for wood products and machinery. Manufacturing activity for nondurable goods was flat for the month as increased output of food/beverage products and paper outweighed drops for most other nondurable goods products. Manufacturing output was 0.2% below year ago levels. This data comes from the Fed’s Industrial Production report, which has overall factory output declining for the 3rd time in 4 months (-0.4%) and being down 1.4% from a year earlier. Mining output (e.g., oil, coal) eked out a 0.2% gain following 8 consecutive monthly declines that left the measure 11.5% below year ago levels. Output at utilities fell for the 3rd time in 4 months with a 1.0% drop. Factory utilization slowed by 4/10ths of a percentage point to 74.9%–the same measure for the manufacturing sector also shed 4/10ths of a percentage point to 74.8%.

Retail sales have been decent this spring. The Census Bureau estimates retail sales during May were at $455.6 billion on a seasonally adjusted basis, up 0.5% for the month and 2.5% from a year earlier. Some of the gain was the result of higher gasoline prices (the index is not adjusted for price variations) with sales at gas stations growing 2.1%. Net of sales at gas stations and at auto and parts dealers (where sales were up 0.5% for the month), core retail sales gained 0.3%, its 4th straight monthly increase. The biggest sales gains were at sporting goods/hobby stores (+1.3%), apparel retailers (+0.8%), restaurants/bars (+0.8%), and health/personal care stores (+0.6%). Sales slowed 1.8% at building materials retailers and 0.9% at department stores. Nonstore retailers (e.g., web retailers) enjoyed a 1.8% gain in sales during May, with activity up 12.2% from a year earlier.

Retail sales have been decent this spring. The Census Bureau estimates retail sales during May were at $455.6 billion on a seasonally adjusted basis, up 0.5% for the month and 2.5% from a year earlier. Some of the gain was the result of higher gasoline prices (the index is not adjusted for price variations) with sales at gas stations growing 2.1%. Net of sales at gas stations and at auto and parts dealers (where sales were up 0.5% for the month), core retail sales gained 0.3%, its 4th straight monthly increase. The biggest sales gains were at sporting goods/hobby stores (+1.3%), apparel retailers (+0.8%), restaurants/bars (+0.8%), and health/personal care stores (+0.6%). Sales slowed 1.8% at building materials retailers and 0.9% at department stores. Nonstore retailers (e.g., web retailers) enjoyed a 1.8% gain in sales during May, with activity up 12.2% from a year earlier.

Homebuilders’ optimism is improving while housing starts hold steady. The Census Bureau reports housing starts slipped 0.3% during May to a seasonally adjusted annualized rate (SAAR) of 1.164 million units. Even with the small decline, housing starts were 9.5% above year ago levels. During the month, starts of single-family homes edged up 0.3% while those of multi-family homes slowed 1.2%. Looking towards the future, the SAAR of issued housing permits increased 0.7% to 1.138 million permits, fueled by a 5.9% bump in the count of issued permits for multifamily homes (Single-family home permits declined 2.0% during the month). Even with the gain, the number of issued permits was 10.1% below year ago levels (although single-family home permits were 4.8% above year ago levels). Total housing completions were at 988,000 units (SAAR), up 5.1% for the month but 3.5% under the year ago pace.

Homebuilders’ optimism is improving while housing starts hold steady. The Census Bureau reports housing starts slipped 0.3% during May to a seasonally adjusted annualized rate (SAAR) of 1.164 million units. Even with the small decline, housing starts were 9.5% above year ago levels. During the month, starts of single-family homes edged up 0.3% while those of multi-family homes slowed 1.2%. Looking towards the future, the SAAR of issued housing permits increased 0.7% to 1.138 million permits, fueled by a 5.9% bump in the count of issued permits for multifamily homes (Single-family home permits declined 2.0% during the month). Even with the gain, the number of issued permits was 10.1% below year ago levels (although single-family home permits were 4.8% above year ago levels). Total housing completions were at 988,000 units (SAAR), up 5.1% for the month but 3.5% under the year ago pace.

The National Association of Home Builders’ (NAHB) measure of builder confidence, the Housing Market Index (HMI), added 2 points during June to a seasonally adjusted reading of 60. This was the HMI’s best reading since January and the 24th straight month with a reading above 50 (indicative of a greater percentage of homebuilders characterizing the housing market as “good” as opposed to being “poor.”) The index improved in 3 of 4 Census regions—South (64), Northeast (39) and West (64)—but slipped in the Midwest (56). The index for current sales of single-family homes grew by a point to 64 while the expectations index surged 5 points to match the post-recession high of 70 attained several times last year. The index measuring traffic of prospective buyers gained 3 points to 47, its best reading of 2016. The press release noted that homebuilders were seeing “higher traffic and more committed buyers.”

Both consumer and wholesale prices perk up in May. The Bureau of Labor Statistics estimates the Consumer Price Index (CPI) increased 0.3% on a seasonally adjusted basis during the month, its 3rd consecutive monthly gain. Also rising for a 3rd straight month were energy prices (+1.2%), reflecting higher prices for fuel oil (+6.2%), gasoline (+2.3%), and utility delivered natural gas (+1.7%). Food prices declined for the 2nd time in 3 months (-0.2%), pulled down by a 0.5% in prices for food at home (e.g., groceries). Net of energy and food, core consumer prices increased 0.2%, with gains in prices for apparel, medical care services, shelter, and transportation prices. Meanwhile, prices new and used cars, along with medical care commodities, declined during the month. Even with the recent gains, CPI has grown only 1.0% over the past year, while the core prices have risen 2.2% over the past year, the 7th month in which the 12-mnth comparable has been at or above 2.0%.

Both consumer and wholesale prices perk up in May. The Bureau of Labor Statistics estimates the Consumer Price Index (CPI) increased 0.3% on a seasonally adjusted basis during the month, its 3rd consecutive monthly gain. Also rising for a 3rd straight month were energy prices (+1.2%), reflecting higher prices for fuel oil (+6.2%), gasoline (+2.3%), and utility delivered natural gas (+1.7%). Food prices declined for the 2nd time in 3 months (-0.2%), pulled down by a 0.5% in prices for food at home (e.g., groceries). Net of energy and food, core consumer prices increased 0.2%, with gains in prices for apparel, medical care services, shelter, and transportation prices. Meanwhile, prices new and used cars, along with medical care commodities, declined during the month. Even with the recent gains, CPI has grown only 1.0% over the past year, while the core prices have risen 2.2% over the past year, the 7th month in which the 12-mnth comparable has been at or above 2.0%.

Meanwhile, the Producer Price Index (PPI) jumped 0.4% during, its largest single-month gain since January. Producer prices for final demand goods increased 0.7%, its biggest increase in a year. Driving the gain was a 2.8% surge in wholesale energy prices (+2.8%), with PPI for gasoline swelling 6.6%. PPI for final demand food goods gained 0.3% (its 1st increase since January), pulled up by higher prices for fresh/dry vegetables and oilseeds. Net of energy and food, prices for final demand core goods grew 0.3% for a 2nd consecutive month. PPI for final demand services increased 0.2%, as the measure for trade prices—essentially margins for retailers and wholesalers—gained 1.1%. Final demand PPI was unchanged over the past year while wholesale prices for core goods were up a modest 0.7% from May 2015 levels.

Other data released over the past week that you might find of interest:

– Jobless Claims (week ending June 11, 2016, First-Time Claims, seasonally adjusted): 277,000 (+13,000 vs. previous week; +6,000 vs. the same week a year earlier). 4-week moving average: 269,250 (-2.6% vs. the same week a year earlier).

– NFIB Small Business Optimism Survey (May 2016, Index (100=1986), seasonally adjusted): 93.8 (2/10th of a point vs. April 2016, down 4.1 points from May 2015).

– Manpower Employment Outlook Survey (3rd Quarter 2016, Net Percentage of Employers Planning to Add Workers, seasonally adjusted): +15% (vs. +16 in 2016Q2, vs. +16% in 2015Q3).

– Import Prices (May 2016, not seasonally adjusted): +1.4% vs. April 2016, -5.0% vs. May 2015; nonfuel import prices: +0.3% vs. April 2016, -1.7% vs. May 2015).

– Export Prices (May 2016, not seasonally adjusted): +1.1% vs. April 2016, -4.5% vs. May 2015; nonagricultural export price: +1.0% vs. April 2016, -4.4% vs. May 2015).

The opinions expressed here are not necessarily those of Kevin’s current and previous employers. No endorsements are implied.