October job gains well outpaced those of previous months, but manufacturing continues to struggle. Here are the 5 things we learned from U.S. economic data released during the week ending November 6.

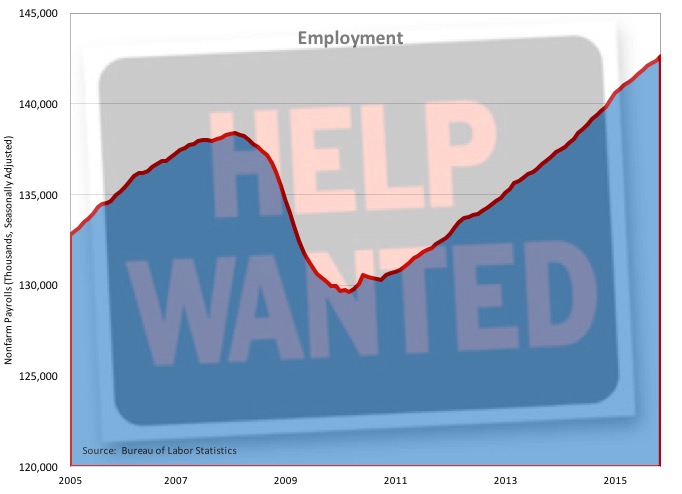

October was the best month for job creation thus far in 2015. The Bureau of Labor Statistics estimates nonfarm payrolls grew by 271,000 during the month. This was the most jobs added since last December and follows two months of smaller job gains. Private sector employers expanded their payrolls by 268,000, split between 241,000 in the service sector and 27,000 in the goods producing side of the economy. Industries adding the most jobs during the month were professional/business services (+78,000, including 24,500 in temporary help services), health care/social assistance (+56,700), retail (43,800), leisure/hospitality (+41,000) and construction (+31,000). Meanwhile, government payrolls expanded by only 3,000 jobs. Average weekly earnings were at $869.40, up a still tepid 2.2% from a year earlier.

October was the best month for job creation thus far in 2015. The Bureau of Labor Statistics estimates nonfarm payrolls grew by 271,000 during the month. This was the most jobs added since last December and follows two months of smaller job gains. Private sector employers expanded their payrolls by 268,000, split between 241,000 in the service sector and 27,000 in the goods producing side of the economy. Industries adding the most jobs during the month were professional/business services (+78,000, including 24,500 in temporary help services), health care/social assistance (+56,700), retail (43,800), leisure/hospitality (+41,000) and construction (+31,000). Meanwhile, government payrolls expanded by only 3,000 jobs. Average weekly earnings were at $869.40, up a still tepid 2.2% from a year earlier.

The separate survey of households has the unemployment rate dropping 1/10th of a point to 5.0%,

The separate survey of households has the unemployment rate dropping 1/10th of a point to 5.0%,

its lowest reading since April 2008. 313,000 people entered the labor force during the month, yet the labor force participation rate remained at a 38-year low of 62.4%. On the positive side, metrics that fell to post-recession lows include the count of “involuntary” part-time workers falling by 269,000 to 5.767 million, the median length of unemployment declining by 2/10ths of a week to 11.2 weeks and the broadest measure of labor underutilization (U-6) slipping 2/10ths of a point to 9.8%. Is this the final shoe to drop that sets up the Fed to make a move next month? Perhaps, but remember there will be one more employment report before the Federal Open Market Committee meets in mid-December.

The trade deficit narrowed in September. The Census Bureau/Bureau of Economic Analysis reports the U.S. trade deficit contracted by $7.2 billion to a seasonally adjusted -$40.8 billion, it smallest reading since February. Exports expanded by $3.0 billion to $187.9 billion, which was nevertheless down 3.7% from a year earlier thanks to the strong U.S. dollar and weak international demand. Imports slipped $1.3 billion to $228.7 billion (-4.0% vs. September 2014). The goods deficit shrank by $7.3 billion to -$60.3 billion led by increased exports of consumer goods and capital goods in addition to declines in imports of industrial supplies and civilian goods. The services surplus held steady at +$19.5 billion. Based on 2009 dollars, the “real” trade deficit of goods contracted by $5.8 billion to -$57.2 billion (+14.5% vs. September 2014).

The trade deficit narrowed in September. The Census Bureau/Bureau of Economic Analysis reports the U.S. trade deficit contracted by $7.2 billion to a seasonally adjusted -$40.8 billion, it smallest reading since February. Exports expanded by $3.0 billion to $187.9 billion, which was nevertheless down 3.7% from a year earlier thanks to the strong U.S. dollar and weak international demand. Imports slipped $1.3 billion to $228.7 billion (-4.0% vs. September 2014). The goods deficit shrank by $7.3 billion to -$60.3 billion led by increased exports of consumer goods and capital goods in addition to declines in imports of industrial supplies and civilian goods. The services surplus held steady at +$19.5 billion. Based on 2009 dollars, the “real” trade deficit of goods contracted by $5.8 billion to -$57.2 billion (+14.5% vs. September 2014).

Manufacturing sputtered once again in September. The Census Bureau estimates new orders for manufactured goods fell 1.0% during the month to a seasonally adjusted $466.3 billion, off 6.9% from a year earlier. The decline in new orders was widespread, with drops of 0.8% and 1.2% for durable and nondurable goods, respectively. Transportation goods orders fell 3.1% as civilian aircraft orders plummeted 36.0%. Yet, net of transportation goods, factory orders were still off 0.6% with declines in orders seen for primary metals (-3.2%), furniture (-2.2%), machinery (-0.9%) and computers/electronic products (-0.5%). Civilian, non-aircraft capital goods orders, a proxy for business investment, experienced a far more modest 0.1% cool down during the month. Shipments fell for the 5th time in 6 months with a 0.4% decline (-5.2% vs. September 2014). Unfilled orders declined for a 2nd straight month (-0.5%) while inventories contracted for a 3rd consecutive month (-0.4%).

Manufacturing sputtered once again in September. The Census Bureau estimates new orders for manufactured goods fell 1.0% during the month to a seasonally adjusted $466.3 billion, off 6.9% from a year earlier. The decline in new orders was widespread, with drops of 0.8% and 1.2% for durable and nondurable goods, respectively. Transportation goods orders fell 3.1% as civilian aircraft orders plummeted 36.0%. Yet, net of transportation goods, factory orders were still off 0.6% with declines in orders seen for primary metals (-3.2%), furniture (-2.2%), machinery (-0.9%) and computers/electronic products (-0.5%). Civilian, non-aircraft capital goods orders, a proxy for business investment, experienced a far more modest 0.1% cool down during the month. Shipments fell for the 5th time in 6 months with a 0.4% decline (-5.2% vs. September 2014). Unfilled orders declined for a 2nd straight month (-0.5%) while inventories contracted for a 3rd consecutive month (-0.4%).

Purchasing managers report continued softness in manufacturing and renewed strength in the service sector in October. The Purchasing Managers Index (PMI) from the Institute for Supply Management lost 1/10th of a point to 50.1. While this was the 34th straight month in which the index was above a reading of 50.0 (and therefore indicating expansion in manufacturing), this was its worst reading in 2.5 years. 3 of 5 index components improved during the month and were above the 50.0 threshold: production, new orders and supplier deliveries. 2 other index components—inventories and employment—both declined during the month and were in contractionary (i.e., with readings below 50.0) territory. Only 7 of 18-tracked industry segments grew during October, led by printing and furniture. The press release noted that survey respondents were concerned about the strong U.S. dollar and the low price of oil, but also indicated there was some “cautious optimism about steady to increasing demand in several industries.”

Purchasing managers report continued softness in manufacturing and renewed strength in the service sector in October. The Purchasing Managers Index (PMI) from the Institute for Supply Management lost 1/10th of a point to 50.1. While this was the 34th straight month in which the index was above a reading of 50.0 (and therefore indicating expansion in manufacturing), this was its worst reading in 2.5 years. 3 of 5 index components improved during the month and were above the 50.0 threshold: production, new orders and supplier deliveries. 2 other index components—inventories and employment—both declined during the month and were in contractionary (i.e., with readings below 50.0) territory. Only 7 of 18-tracked industry segments grew during October, led by printing and furniture. The press release noted that survey respondents were concerned about the strong U.S. dollar and the low price of oil, but also indicated there was some “cautious optimism about steady to increasing demand in several industries.”

Meanwhile, the headline index from the ISM’s Report on Business for the nonmanufacturing sector regained all that it had lost during the previous month with a 2.2 point gain in October to a reading of 59.1 (the 69th straight month above a reading of 50.0). All 4 index components had expansionary readings with 3 of 4—business activity, new orders and employment—improving from their September readings. 14 of 18 industry sectors improved during the month, led by transportation/warehousing, health care/social assistance and professional/scientific/technical services. The press release noted that survey participants “remain mostly positive about business conditions and the overall economy.”

Vehicle sales grew another post-recession high in October. According to automaker sales data collected by Autodata, vehicle sales crept up 0.4% during the month to a seasonally adjusted annualized rate of 18.24 million units. This was up 10.0% from the same month a year earlier. Sales of automobiles grew 1.3% to 8.01 million units (SAAR), which was only 0.4% above the year ago pace. And while sales of light trucks/SUVs slowed 0.2% during the month, the seasonally adjusted annualized sales pace of 10.23 million units was a robust 18.9% above October 2014 sales activity. Most major brands enjoyed double digit percentage sales gains versus a year earlier, including General Motors (+15.9%), Fiat-Chrysler (+14.7%), Ford (+13.4%), Toyota (+13.0%) and Nissan (+12.5%).

Vehicle sales grew another post-recession high in October. According to automaker sales data collected by Autodata, vehicle sales crept up 0.4% during the month to a seasonally adjusted annualized rate of 18.24 million units. This was up 10.0% from the same month a year earlier. Sales of automobiles grew 1.3% to 8.01 million units (SAAR), which was only 0.4% above the year ago pace. And while sales of light trucks/SUVs slowed 0.2% during the month, the seasonally adjusted annualized sales pace of 10.23 million units was a robust 18.9% above October 2014 sales activity. Most major brands enjoyed double digit percentage sales gains versus a year earlier, including General Motors (+15.9%), Fiat-Chrysler (+14.7%), Ford (+13.4%), Toyota (+13.0%) and Nissan (+12.5%).

Other data released over the past week that you might find of interest:

– Jobless Claims (week ending October 31, 2015, seasonally adjusted): 276,000 (+16,000 vs. previous week; -7,000 vs. same week a year earlier). 4-week moving average: 262,750 (-3.7% vs. same week a year earlier).

– Construction Spending (September 2015, seasonally adjusted): +0.6% vs. August 2015; +14.1% vs. September 2014.

– Productivity (3rd Quarter 2015, nonfarm businesses, seasonally adjusted) +1.6% vs. Q2 2015; +0.4% vs. Q3 2014.

– Consumer Credit (September 2015, outstanding balances, seasonally adjusted): $3.499 trillion (+$28.9 billion; +7.1% vs. September 2014).

The opinions expressed here are not necessarily those of Kevin’s current and previous employers. No endorsements are implied.