While housing rebounded in September, 2 measures suggest overall economic activity was weak during the month. Here are the 5 things we learned from U.S. economic data released during the week ending October 23.

Existing home sales rebounded in September following a slowdown in August. The National Association of Realtors estimates sales of previously owned homes gained 4.7% during the month to a seasonally adjusted annualized rate (SAAR) of 5.55 million units, near its post-recession high and up 8.8% from a year earlier. Sales were up in all 4 Census regions on both a month-to-month and year-to-year basis. NAR’s press release speaks of “persistent inventory shortages,” which the data bear out. There were 2.21 million homes available for sale at the end of September, down 2.6% from August and 3.1% from September 2014. This was equivalent to a tight 4.8 month supply, which leads to price pressure in the sector. The median sales price of $221,900 was up 6.1% from the same month a year earlier.

Existing home sales rebounded in September following a slowdown in August. The National Association of Realtors estimates sales of previously owned homes gained 4.7% during the month to a seasonally adjusted annualized rate (SAAR) of 5.55 million units, near its post-recession high and up 8.8% from a year earlier. Sales were up in all 4 Census regions on both a month-to-month and year-to-year basis. NAR’s press release speaks of “persistent inventory shortages,” which the data bear out. There were 2.21 million homes available for sale at the end of September, down 2.6% from August and 3.1% from September 2014. This was equivalent to a tight 4.8 month supply, which leads to price pressure in the sector. The median sales price of $221,900 was up 6.1% from the same month a year earlier.

Housing starts also rebounded in September. The Census Bureau reports housing starts grew 6.5% during the month to a seasonally adjusted annualized rate (SAAR) of 1.132 million units. This was up 17.5% from a year earlier. Starts of single-family homes edged up 0.3% to 740,000 units (SAAR) while starts of multi-family units surged 18.3% to 466,000 units (note that the multi-family unit data series is more volatile in comparison to the single-family home data series). Looking forward, the number of issued building permits fell 5.0% to 1.161 million permits (SAAR). Even with the drop, this was 4.7% above the count of issued permits from a year earlier. Meanwhile, completions grew 7.5% during September to 1.028 million units (SAAR), its highest reading since November 2007.

Housing starts also rebounded in September. The Census Bureau reports housing starts grew 6.5% during the month to a seasonally adjusted annualized rate (SAAR) of 1.132 million units. This was up 17.5% from a year earlier. Starts of single-family homes edged up 0.3% to 740,000 units (SAAR) while starts of multi-family units surged 18.3% to 466,000 units (note that the multi-family unit data series is more volatile in comparison to the single-family home data series). Looking forward, the number of issued building permits fell 5.0% to 1.161 million permits (SAAR). Even with the drop, this was 4.7% above the count of issued permits from a year earlier. Meanwhile, completions grew 7.5% during September to 1.028 million units (SAAR), its highest reading since November 2007.

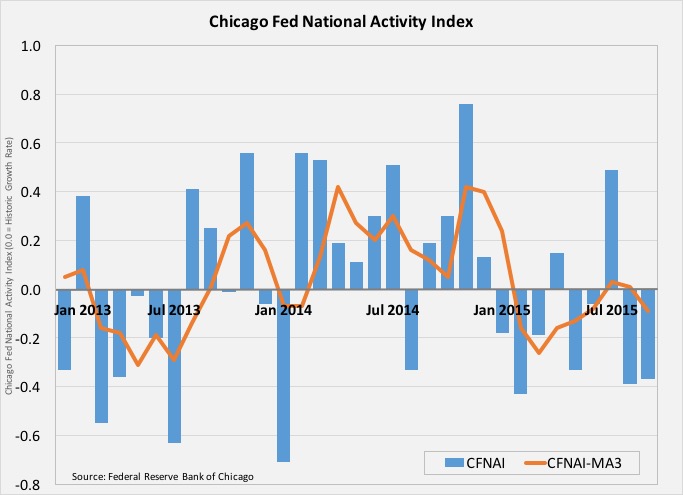

The U.S. economy grew at a slower than normal pace during September. The Chicago Fed National Activity Index (CFNAI) improved by 2-basis points during the month but remained negative for a 2nd consecutive month at -0.37. Only 26 of the 85 index components made a positive contribution to the CFNAI while 59 other components made a negative contribution. Among the 4 major categories of index components, those associated

The U.S. economy grew at a slower than normal pace during September. The Chicago Fed National Activity Index (CFNAI) improved by 2-basis points during the month but remained negative for a 2nd consecutive month at -0.37. Only 26 of the 85 index components made a positive contribution to the CFNAI while 59 other components made a negative contribution. Among the 4 major categories of index components, those associated with production/income and sales/orders/inventories improved slightly while those associated with consumption and employment deteriorated by a slow margin. The 3-month moving average shed 10-basis points to -0.09, its lowest reading since May and consistent with “below average” economic growth.

with production/income and sales/orders/inventories improved slightly while those associated with consumption and employment deteriorated by a slow margin. The 3-month moving average shed 10-basis points to -0.09, its lowest reading since May and consistent with “below average” economic growth.

A forward looking measure of economic activity pulled back in September. The Conference Board’s Leading Economic Index shed 2/10ths of a point to 123.5 (2010 = 100). 6 of 10 index components made a positive contribution to the LEI, led by the interest rate spread and jobless claims, while the other 4 components pulled down the index (including stock prices and building permits). The coincident index added 2/10ths of a point to 112.8 (with 3 of 4 index components making a positive contribution) while the lagging index gained 6/10ths of a point to 119.0 (with 5 of 7 components making a positive contribution). The press release indicated that one should not be too concerned about the report’s weakness, saying that the leading index “still suggests economic expansion will continue” at a “moderate” pace.

A forward looking measure of economic activity pulled back in September. The Conference Board’s Leading Economic Index shed 2/10ths of a point to 123.5 (2010 = 100). 6 of 10 index components made a positive contribution to the LEI, led by the interest rate spread and jobless claims, while the other 4 components pulled down the index (including stock prices and building permits). The coincident index added 2/10ths of a point to 112.8 (with 3 of 4 index components making a positive contribution) while the lagging index gained 6/10ths of a point to 119.0 (with 5 of 7 components making a positive contribution). The press release indicated that one should not be too concerned about the report’s weakness, saying that the leading index “still suggests economic expansion will continue” at a “moderate” pace.

Jobless claims inched up but remained at a 42 year low. According to the Department of Labor, there were 259,000 first-time claims made for unemployment insurance benefits on a seasonally adjusted basis during the week ending October 17. This was up 3,000 claims from the previous week but below the 287,000 count from the same week a year earlier. The 4-week moving average contracted by 2,000 to 263,250, its lowest point since December 15, 1973(!). A year ago, the moving average was at 285,000. The count of people receiving some form of unemployment insurance benefits during the week of October 10 was 2.170 million, up 6,000 from the previous week. The 4-week moving average of 2.185 million was down 9.1% from the same week a year earlier.

Jobless claims inched up but remained at a 42 year low. According to the Department of Labor, there were 259,000 first-time claims made for unemployment insurance benefits on a seasonally adjusted basis during the week ending October 17. This was up 3,000 claims from the previous week but below the 287,000 count from the same week a year earlier. The 4-week moving average contracted by 2,000 to 263,250, its lowest point since December 15, 1973(!). A year ago, the moving average was at 285,000. The count of people receiving some form of unemployment insurance benefits during the week of October 10 was 2.170 million, up 6,000 from the previous week. The 4-week moving average of 2.185 million was down 9.1% from the same week a year earlier.

Other data released over the past week that you might find of interest:

– FHFA House Price Index (August 2015, seasonally adjusted): +0.3% vs. July, +5.5% vs. August 2014.

– Regional & State Employment (September 2015): Nonfarm payrolls grew in 20 states and the District of Columbia, fell in 27 and remained the same in 3 others vs. August 2015.

The opinions expressed here are not necessarily those of Kevin’s current and previous employers. No endorsements are implied.