Job creation slowed in August while one measure of manufacturing activity turned negative. Here are the five things we learned from U.S. economic data released during the week ending September 6.

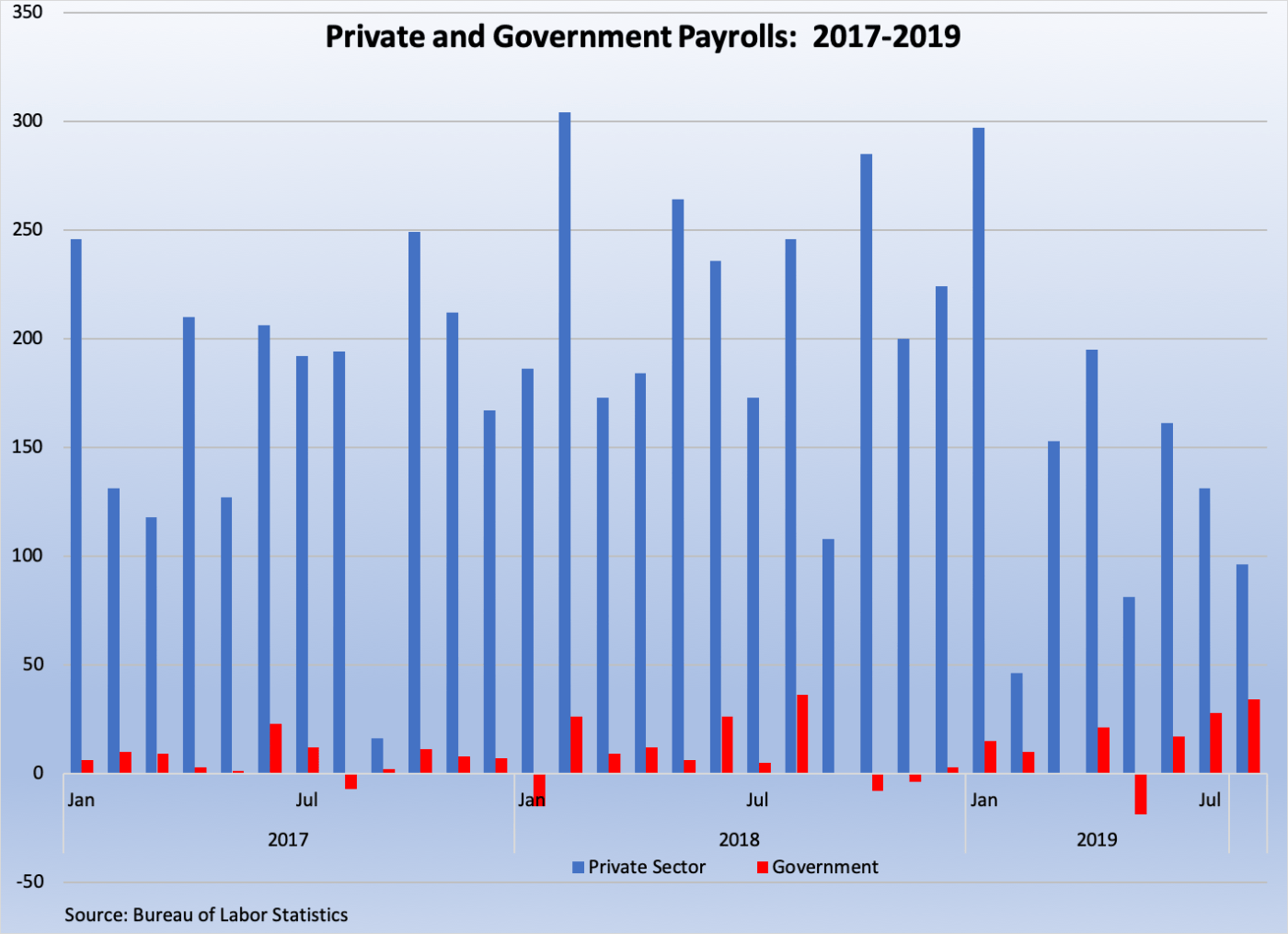

Private-sector payrolls growth decelerated in August. The Bureau of Labor Statistics tells us that nonfarm payrolls grew by a seasonally adjusted 130,000 during the month, off from the downwardly revised gains in June and July of 178,000 and 159,000, respectively. The expansion in payrolls also is a bit misleading as 25,000 of net gain is the result of temporary federal government hires to support the 2020 Census. The private sector added 96,000 workers, down from July’s 131,000 net gain and the fewest since May. The industries adding the most jobs in August were professional/business services (+37,000), health care/social assistance (+36,800), financial activities (+15,000), construction (+14,000), and leisure/hospitality (+12,000). Average weekly earnings of $966.98 represented a 2.9 percent increase from a year earlier.

Private-sector payrolls growth decelerated in August. The Bureau of Labor Statistics tells us that nonfarm payrolls grew by a seasonally adjusted 130,000 during the month, off from the downwardly revised gains in June and July of 178,000 and 159,000, respectively. The expansion in payrolls also is a bit misleading as 25,000 of net gain is the result of temporary federal government hires to support the 2020 Census. The private sector added 96,000 workers, down from July’s 131,000 net gain and the fewest since May. The industries adding the most jobs in August were professional/business services (+37,000), health care/social assistance (+36,800), financial activities (+15,000), construction (+14,000), and leisure/hospitality (+12,000). Average weekly earnings of $966.98 represented a 2.9 percent increase from a year earlier.

A separate survey of households keeps the unemployment rate at 3.7 percent for a third consecutive month. The labor force expanded by a robust 590,000 people, translating into a labor force participation rate of 63.2 percent. The same measure for adults aged 25-54 jumped by 6/10ths of a percentage point to 82.6 percent (tying the post-recession high achieved back in January). The median length of unemployment held steady at 8.9 weeks (August 2018: 9.4 weeks) while the count of part-time workers seeking a full-time job grew by 397,000 to 4.381 million (August 2018: 4.368 million). Finally, the broadest measure of labor underutilization from the BLS (the “U-6” series) increased by 2/10ths of a point to 7.2 percent (August 2018: 7.4 percent).

The trade picture improved slightly in July. The Census Bureau and the Bureau of Economic Analysis estimate exports increased by $1.2 billion to a seasonally adjusted $207.5 billion (-0.6 percent versus July 2018) while imports slowed by $0.4 billion to $261.4 billion (virtually unchanged from a year earlier). The resulting deficit of -$54.0 billion was $1.5 billion smaller than that of June but also was 2.9 percent greater than that of a year earlier. Over the first seven months of 2019, the trade deficit has totaled -$373.8 billion, 8.2 percent greater than the gap from the first seven months of 2018. The goods deficit fell by $1.6 billion to -$73.6 billion while the services surplus shrank by $0.1 billion to +$19.7 billion. The U.S. had its largest goods deficits with China, the European Union, and Mexico.

The trade picture improved slightly in July. The Census Bureau and the Bureau of Economic Analysis estimate exports increased by $1.2 billion to a seasonally adjusted $207.5 billion (-0.6 percent versus July 2018) while imports slowed by $0.4 billion to $261.4 billion (virtually unchanged from a year earlier). The resulting deficit of -$54.0 billion was $1.5 billion smaller than that of June but also was 2.9 percent greater than that of a year earlier. Over the first seven months of 2019, the trade deficit has totaled -$373.8 billion, 8.2 percent greater than the gap from the first seven months of 2018. The goods deficit fell by $1.6 billion to -$73.6 billion while the services surplus shrank by $0.1 billion to +$19.7 billion. The U.S. had its largest goods deficits with China, the European Union, and Mexico.

Purchasing managers tell us manufacturing slowed in August. The PMI, the headline index from the Institute for Supply Management’s Manufacturing Report on Business, shed 2.1 points during the month to a reading of 49.1. This was the first time in nearly three years in which the PMI fell below a reading of 50.0, indicative of contracting manufacturing sector. Four of five PMI components fell during the month: employment (down 4.3 points), new orders (down 3.6 points), supplier deliveries (down 1.9 points), and production (down 1.3 points). The component for inventories eked out a small gain. Only nine of 18-tracked manufacturing industries reported growth, led by textiles, furniture, and food/beverage/tobacco. The press release noted survey respondents’ comments indicating that “trade remains the most significant issue,” reflected by declining export orders and negative supply chain impacts.

Purchasing managers tell us manufacturing slowed in August. The PMI, the headline index from the Institute for Supply Management’s Manufacturing Report on Business, shed 2.1 points during the month to a reading of 49.1. This was the first time in nearly three years in which the PMI fell below a reading of 50.0, indicative of contracting manufacturing sector. Four of five PMI components fell during the month: employment (down 4.3 points), new orders (down 3.6 points), supplier deliveries (down 1.9 points), and production (down 1.3 points). The component for inventories eked out a small gain. Only nine of 18-tracked manufacturing industries reported growth, led by textiles, furniture, and food/beverage/tobacco. The press release noted survey respondents’ comments indicating that “trade remains the most significant issue,” reflected by declining export orders and negative supply chain impacts.

…But they also report that service sector activity picked up over the same time. The NMI, the headline index for the Non-Manufacturing Report on Business, ticked up 2.7 points to a reading of 56.4. This was the NMI’s 115th consecutive month with a reading above 50.0 and its best reading since May. Only two of four NMI components increased in August—business activity and new orders—while measures for employment and supplier deliveries each slumped. Sixteen of 18-tracked industries expanded during the month, led by real estate, accommodation/food services, and public administration. The press release noted continued concerns “about tariffs and geopolitical uncertainty,” but also that survey respondents were “mostly positive about business conditions.”

…But they also report that service sector activity picked up over the same time. The NMI, the headline index for the Non-Manufacturing Report on Business, ticked up 2.7 points to a reading of 56.4. This was the NMI’s 115th consecutive month with a reading above 50.0 and its best reading since May. Only two of four NMI components increased in August—business activity and new orders—while measures for employment and supplier deliveries each slumped. Sixteen of 18-tracked industries expanded during the month, led by real estate, accommodation/food services, and public administration. The press release noted continued concerns “about tariffs and geopolitical uncertainty,” but also that survey respondents were “mostly positive about business conditions.”

Even with the news from above, new factory orders grew in July. The Census Bureau reports that new orders for manufactured goods increased 1.4 percent to a seasonally adjusted $500.3 billion. Even though this was the second consecutive monthly increase, factory orders over the first seven months of the year were tracking only 0.4 percent ahead of that from the same months a year earlier. As we learned last week, transportation orders were a significant driver of the increased orders, jumping 7.0 percent thanks to surges for both civilian (+47.8 percent) and defense (+34.3 percent) aircraft. Durable goods orders jumped 2.0 percent while those of nondurables gained 0.8 percent. Orders of civilian non-aircraft capital goods—a proxy for business investment—increased 0.2 percent in July. Shipments fell for the first time in three months with a 0.2 percent decline to $504.0 billion while unfilled orders mostly held steady after three monthly declines at $1.162 trillion. Inventories expanded for the 11th time over the past 12 months by growing 0.2 percent to $696.5 billion.

Even with the news from above, new factory orders grew in July. The Census Bureau reports that new orders for manufactured goods increased 1.4 percent to a seasonally adjusted $500.3 billion. Even though this was the second consecutive monthly increase, factory orders over the first seven months of the year were tracking only 0.4 percent ahead of that from the same months a year earlier. As we learned last week, transportation orders were a significant driver of the increased orders, jumping 7.0 percent thanks to surges for both civilian (+47.8 percent) and defense (+34.3 percent) aircraft. Durable goods orders jumped 2.0 percent while those of nondurables gained 0.8 percent. Orders of civilian non-aircraft capital goods—a proxy for business investment—increased 0.2 percent in July. Shipments fell for the first time in three months with a 0.2 percent decline to $504.0 billion while unfilled orders mostly held steady after three monthly declines at $1.162 trillion. Inventories expanded for the 11th time over the past 12 months by growing 0.2 percent to $696.5 billion.

Other U.S. economic data released over the past week:

– Jobless Claims (week ending August 31, 2019, First-Time Claims, seasonally adjusted): 217,000 (+1,000 vs. previous week; +7,000 vs. the same week a year earlier). 4-week moving average: 216.250 (+1.3% vs. the same week a year earlier).

– Productivity (2019Q2, Nonfarm Business Labor Productivity, seasonally adjusted annualized rate): +2.3% vs. 2019Q1, +1.8% vs. 2018Q2.

– Construction Spending (July 2019, Value of Construction Put in Place, seasonally adjusted annualized rate): $1.289 trillion (+0.1% vs. June 2019, -2.7% vs. July 2018).

– Beige Book

The opinions expressed here are not necessarily those of Kevin’s current employer. No endorsements are implied.