The U.S. economy expanded at a tepid pace in early 2017 while the housing market paused in April. Here are the 5 things we learned from U.S. economic data released during the week ending May 26.

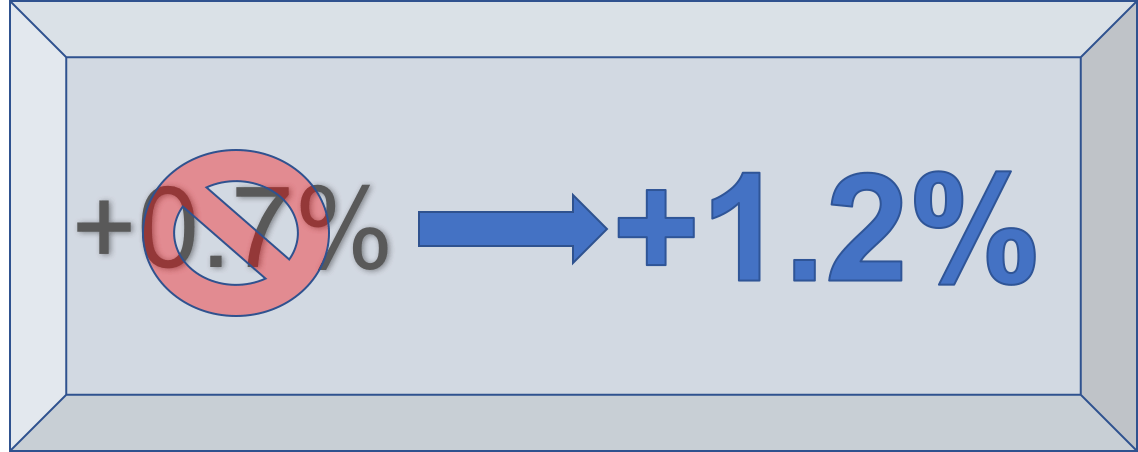

Even with an upward revision, the U.S. economy expanded at a slow pace during the opening months of 2017. The Bureau of Economic Analysis revised its estimate of first-quarter growth in the Gross Domestic Product (GDP) from a seasonally adjusted annualized growth rate of 0.7 percent to a gain of 1.2 percent. The weak Q1 GDP gain followed a 2.1 percent annualized increase in economic activity during the final three months of 2016. The Q1 GDP revision was the result of higher than previously believed levels of nonresidential fixed investment, personal spending, and state & local government spending (although pulling down the estimate was a lowered estimate of private inventory accumulation during the quarter). Nevertheless, the updated GDP estimate still presents a similar story of what had been reported a month ago: a sharp slowdown in the growth of personal consumption expenditure resulted in the smallest growth in economic activity in a year. Consumption added 44-basis points to GDP growth during Q1 after having contributed 240-basis points to Q4 2016 growth. Most of Q1’s economic growth instead came from fixed investment, with residential and nonresidential fixed economic responsible for 50-basis points and 134-basis points of economic growth during the quarter, respectively. This report also presented the first glimpse of corporate profits, which were at a seasonally adjusted annualized rate of $2.110 trillion. This was off 1.9 percent from the final three months 2016 but up 3.7 percent from Q1 2016. The BEA will revise its GDP estimate once again on June 29.

Even with an upward revision, the U.S. economy expanded at a slow pace during the opening months of 2017. The Bureau of Economic Analysis revised its estimate of first-quarter growth in the Gross Domestic Product (GDP) from a seasonally adjusted annualized growth rate of 0.7 percent to a gain of 1.2 percent. The weak Q1 GDP gain followed a 2.1 percent annualized increase in economic activity during the final three months of 2016. The Q1 GDP revision was the result of higher than previously believed levels of nonresidential fixed investment, personal spending, and state & local government spending (although pulling down the estimate was a lowered estimate of private inventory accumulation during the quarter). Nevertheless, the updated GDP estimate still presents a similar story of what had been reported a month ago: a sharp slowdown in the growth of personal consumption expenditure resulted in the smallest growth in economic activity in a year. Consumption added 44-basis points to GDP growth during Q1 after having contributed 240-basis points to Q4 2016 growth. Most of Q1’s economic growth instead came from fixed investment, with residential and nonresidential fixed economic responsible for 50-basis points and 134-basis points of economic growth during the quarter, respectively. This report also presented the first glimpse of corporate profits, which were at a seasonally adjusted annualized rate of $2.110 trillion. This was off 1.9 percent from the final three months 2016 but up 3.7 percent from Q1 2016. The BEA will revise its GDP estimate once again on June 29.

On the bright side, economic activity appears to have sped up during April. The Chicago Fed National Activity Index, a weighted average of 85 economic measures, jumped by 42-basis points during the month to a reading of +0.49. This was the measure’s highest point since November 2014. The surge was largely the result of a 45-basis point improvement in the index components tied to production (to a +0.46 contribution to the CFNAI). Also improving during April were CFNAI components linked to employment, with a five-basis point increase to +0.10. Slipping from their March performance were index components tied to sales/orders/inventories (down seven basis points to a neutral contribution of 0.00) and the personal consumption/housing categories of index components (shedding two basis points to -0.06). In all, 46 of the CFNAI’s 85 components made positive contributions to the index. The CFNAI’s three-month moving average grew by 23-basis points to a reading of +0.23. A reading above 0.00 for the moving average is consistent with an economy that is expanding faster than its historical average.

On the bright side, economic activity appears to have sped up during April. The Chicago Fed National Activity Index, a weighted average of 85 economic measures, jumped by 42-basis points during the month to a reading of +0.49. This was the measure’s highest point since November 2014. The surge was largely the result of a 45-basis point improvement in the index components tied to production (to a +0.46 contribution to the CFNAI). Also improving during April were CFNAI components linked to employment, with a five-basis point increase to +0.10. Slipping from their March performance were index components tied to sales/orders/inventories (down seven basis points to a neutral contribution of 0.00) and the personal consumption/housing categories of index components (shedding two basis points to -0.06). In all, 46 of the CFNAI’s 85 components made positive contributions to the index. The CFNAI’s three-month moving average grew by 23-basis points to a reading of +0.23. A reading above 0.00 for the moving average is consistent with an economy that is expanding faster than its historical average.

Sales of previously owned homes took a breather during April. Per the National Association of Realtors, existing home sales declined 2.3 percent during the month to a seasonally adjusted annualized rate (SAAR) of 5.57 million units. Sales decreased during April in the South (-5.0 percent), West (-3.3 percent), and Northeast (-2.7 percent), but improved in Midwest (+3.8 percent). Existing home sales were 1.6 percent above their April 2016 pace. There was a 4.2 month supply of homes on the market at the end of April, its highest point since last October. However, the 1.93 million homes available for sale at the end of April was 9.0 percent below that of a year earlier. As a result, the median sales price of $244,800 was 6.0 percent above that of a year earlier. NAR’s press release linked the slowdown in home sales to “new and existing inventory…not keeping up with the fast pace homes are coming off the market.”

Sales of previously owned homes took a breather during April. Per the National Association of Realtors, existing home sales declined 2.3 percent during the month to a seasonally adjusted annualized rate (SAAR) of 5.57 million units. Sales decreased during April in the South (-5.0 percent), West (-3.3 percent), and Northeast (-2.7 percent), but improved in Midwest (+3.8 percent). Existing home sales were 1.6 percent above their April 2016 pace. There was a 4.2 month supply of homes on the market at the end of April, its highest point since last October. However, the 1.93 million homes available for sale at the end of April was 9.0 percent below that of a year earlier. As a result, the median sales price of $244,800 was 6.0 percent above that of a year earlier. NAR’s press release linked the slowdown in home sales to “new and existing inventory…not keeping up with the fast pace homes are coming off the market.”

Sales of new homes sagged during April. The Census Bureau reports that new home sales fell 11.4 percent during the month to a seasonally adjusted annualized rate (SAAR) of 569,000 units. This was still 0.5 percent above the year-ago sales rate of new homes. Sales dropped in all four Census regions during the month, led by sharp declines in both the West (-26.3 percent) and Midwest (-13.1 percent). On a year-to-year basis, new home sales had grown in the Midwest (+19.7 percent) and South (+4.1 percent) but had slowed in both the West (-13.7 percent) and Northeast (-5.1 percent). Inventories of unsold new homes expanded 1.5 percent to 268,000 units. This was the equivalent to a 5.7 month supply.

Sales of new homes sagged during April. The Census Bureau reports that new home sales fell 11.4 percent during the month to a seasonally adjusted annualized rate (SAAR) of 569,000 units. This was still 0.5 percent above the year-ago sales rate of new homes. Sales dropped in all four Census regions during the month, led by sharp declines in both the West (-26.3 percent) and Midwest (-13.1 percent). On a year-to-year basis, new home sales had grown in the Midwest (+19.7 percent) and South (+4.1 percent) but had slowed in both the West (-13.7 percent) and Northeast (-5.1 percent). Inventories of unsold new homes expanded 1.5 percent to 268,000 units. This was the equivalent to a 5.7 month supply.

Consumer confidence remained strong during May, although one’s political views greatly influenced their outlook. The Index of Consumer Sentiment from the University of Michigan inched up 1/10th of a point during the month to a seasonally adjusted reading of 97.1. The same measure was at 94.7 one year ago and was in line with its six-month average of 97.3. The current conditions index dropped by a full point to 111.7 (May 2016: 109.9) while the expectations index added 7/10ths of a point to 87.7 (May 2016: 84.9). The press release noted that the recent pattern of a sharp partisan divide remained, with survey participants that identify themselves as Republicans indicating great optimism and those that are Democrats being particularly pessimistic. 84 percent of Republicans reported “favorable” news about recent economic developments, compared to a mere 37 percent of Democrats. Conversely, 73 percent of Democrats described “unfavorable” economic news versus only 19 percent of Republicans. The press release also stated that the survey results suggested real personal spending would grow 2.3 percent during 2017.

Consumer confidence remained strong during May, although one’s political views greatly influenced their outlook. The Index of Consumer Sentiment from the University of Michigan inched up 1/10th of a point during the month to a seasonally adjusted reading of 97.1. The same measure was at 94.7 one year ago and was in line with its six-month average of 97.3. The current conditions index dropped by a full point to 111.7 (May 2016: 109.9) while the expectations index added 7/10ths of a point to 87.7 (May 2016: 84.9). The press release noted that the recent pattern of a sharp partisan divide remained, with survey participants that identify themselves as Republicans indicating great optimism and those that are Democrats being particularly pessimistic. 84 percent of Republicans reported “favorable” news about recent economic developments, compared to a mere 37 percent of Democrats. Conversely, 73 percent of Democrats described “unfavorable” economic news versus only 19 percent of Republicans. The press release also stated that the survey results suggested real personal spending would grow 2.3 percent during 2017.

Other U.S. economic data released over the past week:

– Jobless Claims (week ending May 20, 2017, First-Time Claims, seasonally adjusted): 234,000 +1,000 vs. previous week; -34,000 vs. the same week a year earlier). 4-week moving average: 235.250 (-14.7% vs. the same week a year earlier).

– Durable Goods (April 2017, New Orders, seasonally adjusted): $231.2 billion (-0.7% vs. March 2017). New orders net of transportation goods: $152.7 billion (-0.4% vs. March 2017).

– FOMC minutes

– FHFA House Price Index (March 2017, Purchase-Only Index, seasonally adjusted): +0.6% vs. February 2017, +6.2% vs. March 2016.

– Wholesale Inventories (March 2017, Inventories of Merchant Wholesalers, seasonally adjusted): $594.6 billion (+0.2% vs. February 2017, +3.0% vs. March 2016).

The opinions expressed here are not necessarily those of Kevin’s current and previous employers. No endorsements are implied.