Another solid payrolls report eliminates virtually any doubt about the action the Fed will take at its next FOMC meeting. Here are the 5 things we learned from U.S. economic data released during the week ending December 4.

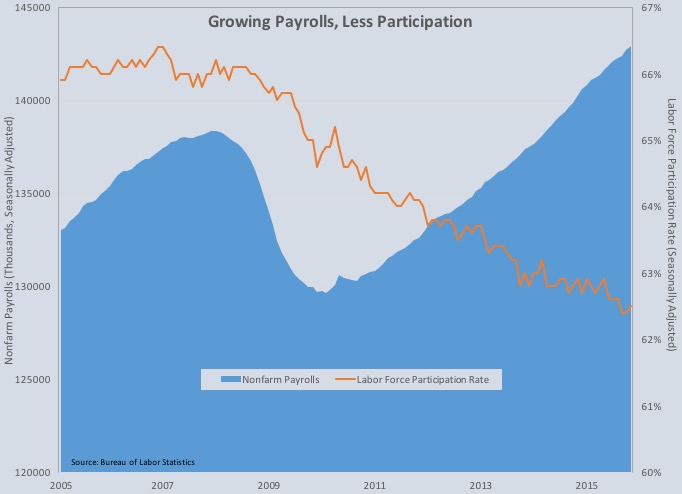

November’s broad-based payrolls gains open the door for the 1st Fed rate hike in nearly 10 years. The Bureau of Labor Statistics estimates nonfarm payrolls expanded by a seasonally adjusted 211,000 during the month. While November’s gain was smaller than the 298,000 jobs pickup in October, the 3-month moving average of 218,000 added jobs was the best seen since July. Private sector employers expanded their payrolls by 197,000 jobs, split by 163,000 jobs in the service sector and 34,000 jobs on the goods producing side of the economy. The job gains were spread through most of the economy with the biggest

November’s broad-based payrolls gains open the door for the 1st Fed rate hike in nearly 10 years. The Bureau of Labor Statistics estimates nonfarm payrolls expanded by a seasonally adjusted 211,000 during the month. While November’s gain was smaller than the 298,000 jobs pickup in October, the 3-month moving average of 218,000 added jobs was the best seen since July. Private sector employers expanded their payrolls by 197,000 jobs, split by 163,000 jobs in the service sector and 34,000 jobs on the goods producing side of the economy. The job gains were spread through most of the economy with the biggest  increases seen in construction (+46,000), leisure/hospitality (+39,000), health care/social assistance (+32,200), retail (+30,700) and professional/business services (+27,000). Employment contracted with temporary help services (-12,300), information (-12,000), mining/logging (-11,000) and durable goods manufacturing (-6,000), with the latter 2 both down for 7th time over the past 8 months. One small bit of caution: the average number of hours worked slipped 1/10th of an hour (vs. both October 2015 and November 2014) to 34.5 hours while average monthly earnings declined by $1.14 to $871.13 (+2.0% vs. November 2014).

increases seen in construction (+46,000), leisure/hospitality (+39,000), health care/social assistance (+32,200), retail (+30,700) and professional/business services (+27,000). Employment contracted with temporary help services (-12,300), information (-12,000), mining/logging (-11,000) and durable goods manufacturing (-6,000), with the latter 2 both down for 7th time over the past 8 months. One small bit of caution: the average number of hours worked slipped 1/10th of an hour (vs. both October 2015 and November 2014) to 34.5 hours while average monthly earnings declined by $1.14 to $871.13 (+2.0% vs. November 2014).

The separate households survey keeps the unemployment rate at a post-recession low of 5.0%. 273,000 people entered the labor force during the month with the labor force participation rate inching up 1/10th of a percentage point to 62.5%. Even with the gain, the participation rate remained near to the 38-year low that we saw during the 2 prior months. The median length of unemployment fell to another post-recession low, with a 4/10ths of a week decline to 10.8 weeks (November 2014: 12.8 weeks) while the count of “involuntary” part-time workers rebounded from October’s decline to 6.086 million workers (November 2014: 6.851 million). Even with a 1/10th of a percentage point increase, the broadest measure of labor underutilization from the BLS (the U-6 series) remained near its post-recession low of 9.9% (November 2014: 11.4%). In all, November’s employment report, while not spectacular, was solid…and that is all the Federal Reserve needed to see to move forward with its plan to bump up the fed funds target rate mid-month.

The trade deficit expanded in October as both exports and imports slowed. The Census Bureau and the Bureau of Economic Analysis report that the U.S. goods and services deficit grew by $1.4 billion during the month to -$43.9 billion (+2.7% vs. October 2014). Exports declined $2.7 billion to $184.1 billion (-6.9% vs October 2014) while imports slowed $1.2 billion to $228.0 billion (-5.2% vs. October 2014). The goods deficit grew by $2.1 billion to $63.1 billion while the services surplus expanded by $0.7 billion to +$19.2 billion. The former included a $1.6 billion drop in industrial supplies/materials exports and a $0.9 billion slowdown in capital goods exports. The “real” goods deficit—based on 2009 chained dollars—grew by $3.0 billion to -$60.3 billion (a whopping 20.8% above the October 2014 reading, reflecting higher non-petroleum imports and lower non-petroleum exports).

The trade deficit expanded in October as both exports and imports slowed. The Census Bureau and the Bureau of Economic Analysis report that the U.S. goods and services deficit grew by $1.4 billion during the month to -$43.9 billion (+2.7% vs. October 2014). Exports declined $2.7 billion to $184.1 billion (-6.9% vs October 2014) while imports slowed $1.2 billion to $228.0 billion (-5.2% vs. October 2014). The goods deficit grew by $2.1 billion to $63.1 billion while the services surplus expanded by $0.7 billion to +$19.2 billion. The former included a $1.6 billion drop in industrial supplies/materials exports and a $0.9 billion slowdown in capital goods exports. The “real” goods deficit—based on 2009 chained dollars—grew by $3.0 billion to -$60.3 billion (a whopping 20.8% above the October 2014 reading, reflecting higher non-petroleum imports and lower non-petroleum exports).

Purchasing managers were less enthusiastic about business conditions, including indicating that manufacturing was contracting during November. The headline index from the Manufacturing Institute for Supply Management’s Report on Business—known as the Purchasing Managers Index (PMI)—shed 1.5 points to 48.6. This was the first time in 36 months in which the index was below a reading of 50.0, which is the threshold between an expanding and contracting manufacturing sector. 3 of 5 index components both were in contraction territory and declined during the month: production (-3.7 point to 49.2), new orders (-3.0 points to 48.9) and inventories (-3.5 points to 46.5). Gaining were indices for employment (+3.7 points to 51.3) and supplier deliveries (up 2/10ths of a point to 50.6). Only 5 of 18-tracked manufacturing segments expanded during the month while 10 others shrank. (Meanwhile, the Census Bureau reported that new factory orders increased 1.5% during October but had remained 4.5% below year ago levels).

Purchasing managers were less enthusiastic about business conditions, including indicating that manufacturing was contracting during November. The headline index from the Manufacturing Institute for Supply Management’s Report on Business—known as the Purchasing Managers Index (PMI)—shed 1.5 points to 48.6. This was the first time in 36 months in which the index was below a reading of 50.0, which is the threshold between an expanding and contracting manufacturing sector. 3 of 5 index components both were in contraction territory and declined during the month: production (-3.7 point to 49.2), new orders (-3.0 points to 48.9) and inventories (-3.5 points to 46.5). Gaining were indices for employment (+3.7 points to 51.3) and supplier deliveries (up 2/10ths of a point to 50.6). Only 5 of 18-tracked manufacturing segments expanded during the month while 10 others shrank. (Meanwhile, the Census Bureau reported that new factory orders increased 1.5% during October but had remained 4.5% below year ago levels).

ISM’s measure of activity in the service sector dropped to its lowest reading since May, with a 3.2 point decline to 55.9. This was, however, the 70th straight month in which in the headline index from the Non-Manufacturing Report on Business was above a reading of 50.0. While all 4 index components were above a reading of 50.0, 3 of 4 declined during the month (business activity, new orders and employment). 12 of 18 tracked industry segments expanded in November while 6 others contracted. The press release noted that most survey “respondents are still positive about business conditions.”

October was another solid month for construction spending. The Census Bureau estimates $1.107 trillion of construction was put in place during the month on a seasonally adjusted annualized basis, up 1.0% from September and 13.0% from the same month a year earlier. This was the 11th straight month (and the 15th time in 16 months) of construction spending growth. Private construction spending grew 0.8% during October to $802.4 billion SAAR, 15.9% above year ago levels. Private residential spending gained 1.0% during the month and was 16.6% above year levels, with double digit percentage 12-month comparables for both new single-family home (+11.4%) and multi-family home (+27.9%) unit construction. Nonresidential construction spending increased 0.6%, with a 12-month comparable of 15.3%—with the largest year-to-year gains in construction spending in manufacturing (+40.5%), amusement/recreation (+35.0%) and lodging (+30.2%). Public sector construction spending was at a SAAR of $298.4 billion, up 1.4% for the month and 6.1% from its October 2014 pace.

October was another solid month for construction spending. The Census Bureau estimates $1.107 trillion of construction was put in place during the month on a seasonally adjusted annualized basis, up 1.0% from September and 13.0% from the same month a year earlier. This was the 11th straight month (and the 15th time in 16 months) of construction spending growth. Private construction spending grew 0.8% during October to $802.4 billion SAAR, 15.9% above year ago levels. Private residential spending gained 1.0% during the month and was 16.6% above year levels, with double digit percentage 12-month comparables for both new single-family home (+11.4%) and multi-family home (+27.9%) unit construction. Nonresidential construction spending increased 0.6%, with a 12-month comparable of 15.3%—with the largest year-to-year gains in construction spending in manufacturing (+40.5%), amusement/recreation (+35.0%) and lodging (+30.2%). Public sector construction spending was at a SAAR of $298.4 billion, up 1.4% for the month and 6.1% from its October 2014 pace.

Light trucks & SUVs kept vehicle sales near a record pace in November. While slipping 0.3% from October’s torrid sales pace, the 18.19 million unit seasonally adjusted annualized sales pace for Autodata’s tabulation of automaker sales report was 6.2% above that of a year earlier. Sales of light trucks were 15.4% above that of a year earlier at 10.38 million units SAAR while the sales pace of automobiles was 4.1% below the November 2014 level of 7.81 million units. Over the 1st 11 months of 2015, vehicle sales totaled 15.015 million units, up 5.4% above sales for the 1st 11 months of 2014.

Light trucks & SUVs kept vehicle sales near a record pace in November. While slipping 0.3% from October’s torrid sales pace, the 18.19 million unit seasonally adjusted annualized sales pace for Autodata’s tabulation of automaker sales report was 6.2% above that of a year earlier. Sales of light trucks were 15.4% above that of a year earlier at 10.38 million units SAAR while the sales pace of automobiles was 4.1% below the November 2014 level of 7.81 million units. Over the 1st 11 months of 2015, vehicle sales totaled 15.015 million units, up 5.4% above sales for the 1st 11 months of 2014.

Other data released over the past week that you might find of interest:

– Jobless Claims (week ending November 28, 2015, seasonally adjusted): 269,000 (+9,000 vs. previous week; -30,000 vs. same week a year earlier). 4-week moving average: 269,250 (-8.7% vs. same week a year earlier).

– Productivity (3rd Quarter 2015—revision, Nonfarm Business, seasonally adjusted): +2.2% vs. Q2 2015, +0.6% vs. Q3 2014.

– Agricultural Prices (October 2015, Prices Received by Farmers): -9.2% vs. September 2015, -11.0% vs. October 2014.

– Pending Home Sales (October 2015, Index: 100 = 2001, seasonally adjusted): 107.7 (+ 0.2 vs. September 2015, +4.0 vs. October 2014).

– Beige Book (December 2015)

The opinions expressed here are not necessarily those of Kevin’s current and previous employers. No endorsements are implied.