Week of June 15-19, 2015

With the weather heating up, you probably didn’t follow U.S. economic data releases over the past week. Here’s what you missed during the week ending June 19.

1. The Federal Reserve did not act last week, but most Fed voting members expect to hike short-term interest rates by the end of the year. The policy statement released following the conclusion of of the Federal Open Market Committee indicated that the U.S. economy had been expanding “moderately” with “the pace of job gains [having] picked up.” The committee also saw housing spending as “moderate” but business investment and exports were “soft” while inflation and salary gains were also “soft.” So, in a surprise to no one, the FOMC kept the fed funds target rate at near zero percent, where it has been since December 2008. But that is about to change.

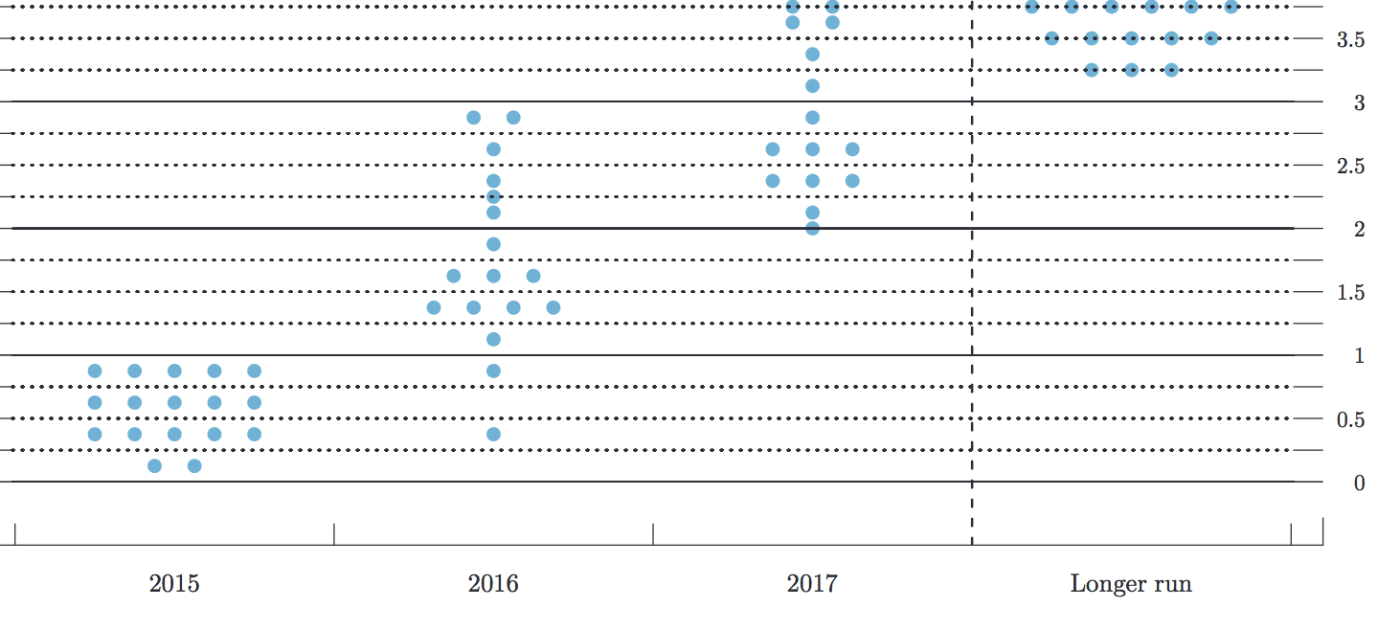

The FOMC policy statement was accompanied by updated economic forecasts from Federal Reserve Board Members and Bank presidents. The median forecast for 2015 economic growth fell from a range of +2.3-2.7% to +1.8%-2.0% (reflecting the soft start to the year), but improved slightly for 2016 (to +2.4-2.7%) and 2017 (to + 2.1-2.5%). The group also sees the unemployment rate slipping to roughly 5-percent for both 2016 and 2017 while inflation remains slightly below its 2-percent target. But even if inflation remains slightly soft, the typical prediction for the fed funds target rate is +0.625 at the end of this year, +1.625 at the end of 2016 and +2.875% at the end of 2017. Note that the forecasted fed funds rate for the end of 2017 is well below the peak before the previous recession of 5.25% (seen during summer of 2006 to the summer of 2007).

2.1-2.5%). The group also sees the unemployment rate slipping to roughly 5-percent for both 2016 and 2017 while inflation remains slightly below its 2-percent target. But even if inflation remains slightly soft, the typical prediction for the fed funds target rate is +0.625 at the end of this year, +1.625 at the end of 2016 and +2.875% at the end of 2017. Note that the forecasted fed funds rate for the end of 2017 is well below the peak before the previous recession of 5.25% (seen during summer of 2006 to the summer of 2007).

2. Factory activity continues to disappoint in 2015. The Federal Reserve’s Industrial Production report finds manufacturing output slipped 0.2% during May following tepid gains of 0.3% and 0.1% in March and April, respectively. Production of nondurable goods fell 0.7%, impacted by a 1.6% drop in output of petroleum and coal products and declines for most other nondurable goods. While durable goods production eked out a 0.2% pick up, much of that was the result of a 1.7% jump in automobile production. Manufacturing output was only 1.8% above year ago levels, the smallest 12-month comparable since January 2014. Manufacturing factory utilization slowed to 77.0%, down 2/10ths of a percentage point from April and its lowest point in 13 months.

3. Housing Starts dropped in May, but the number of issued building permits hit an 8-year high. The Census Bureau estimates there were 1.036 million housing starts on a seasonally adjusted annualized rate during May, off 11.1% from April but still 5.1% above year ago levels. Starts of single-family homes fell 5.4% for the month to 680,000 units (SAAR) while those for multi-family properties plummeted 20.1% to 356,000 units (SAAR). (Note that starts data for multi-family properties tend to be very volatile month-to-month.) Better news is that there were 1.275 million homes (SAAR) authorized by building permits during the month, up 11.8% for the month, 25.4% above year ago levels and the highest count since August 2007. Much of the month-to-month gain was for multi-family units, which enjoyed a 24.9% bump during the month. The same metric for single homes inched up 2.6% during May. The annualized count of housing completions gained 4.7% to 1.034 million units, up 14.5% from May 2014 and its highest reading since November 2008.

Beyond the encouraging permits data, another sign that the softening in starts will be short lived is the Housing Market Index, which added 5 points to a seasonally adjusted 59. This matches the National Association of Home Builders’ measure of homebuilder confidence post-recession peak reading achieved last September. The measure has been above a reading of 50 for 9 consecutive months, indicating more builders see the market as “good” versus seeing it as “poor.” Also improving were indices for current sales of single-family homes (up 7 points to 65), expected sales over the next 6 months (up 6 points to 69) and the traffic of potential buyers (up 5 points to 44). The NAHB’s press release notes that the current and future sales expectations indices “are at their highest levels since the last quarter of 2005, indicating a growing optimism among builders that housing will continue to strengthen in the months ahead.”

4. Rising gasoline prices led to the largest monthly gain in consumer prices in more than 2 years. The Bureau of Labor Statistics estimates the Consumer Price Index (CPI) grew 0.4% during May. Gasoline prices jumped 10.4% on a seasonally adjusted basis during the month, leading to a 4.3% gain in energy prices. Food prices were unchanged during May while core prices (net of both energy and food) inched up 0.1%. For most goods and services categories, prices were relatively stable during the month. Notable exceptions were transportation services (+0.7%), medical care categories (+0.4%), apparel (-0.5%) and used cars/trucks (-0.4%). CPI was unchanged from a year earlier (with energy CPI still 16.3% below year ago levels), while the core index was just below the Fed’s 2% target at +1.7%.

5. The U.S. economy of the second half of 2015 looks stronger than that of the first half. The Leading Economic Index from the Conference Board added 8/10ths of a point to 123.1, with 9 of 10 index components making positive index contributions (led by housing permits and the interest rate spread). With small gains were the concurrent index (up 1/10th of point to 112.1) and the lagging index (up 2/10ths of a point to 117.0). While the press release sees the results as “confirming” a stronger economy during the second half, it also noted that the weak industrial production and manufacturing data as “painting a somewhat more mixed picture.”

- Treasury International Capital Flows: Net foreign purchases of U.S. securities (April 2015): +$41.2 billion

- Jobless claims: Week ending June 13 2015: 267,000 (-12,000)

The opinions expressed here are not necessarily those of Kevin’s current, previous and future employers. No endorsements are implied.