Tight inventories continued to hold back the housing market during the spring.

Tight Inventories, Rising Materials Prices Weigh on Housing: June 18 – 22

What We Learned About the U.S. Economy Last Week

Weekly Economic Update: A brief, non-technical review of the previous week's U.S. economic data releases by Kevin A. Roth, PhD

Tight inventories continued to hold back the housing market during the spring.

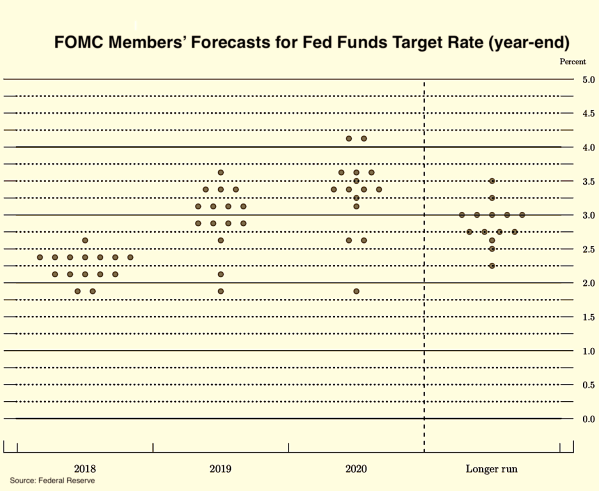

The Fed raises its target for short-term interest rates as inflation moves ever so closer to targeted levels.

The trade deficit narrowed while employers sought even more workers.