As the world considers the economic and political implications of the Brexit vote, we learned last week that U.S. economic activity lagged during the spring.

Business Activity Was Rocky This Spring: What We Learned During the Week of June 20 – 24

What We Learned About the U.S. Economy Last Week

Weekly Economic Update: A brief, non-technical review of the previous week's U.S. economic data releases by Kevin A. Roth, PhD

As the world considers the economic and political implications of the Brexit vote, we learned last week that U.S. economic activity lagged during the spring.

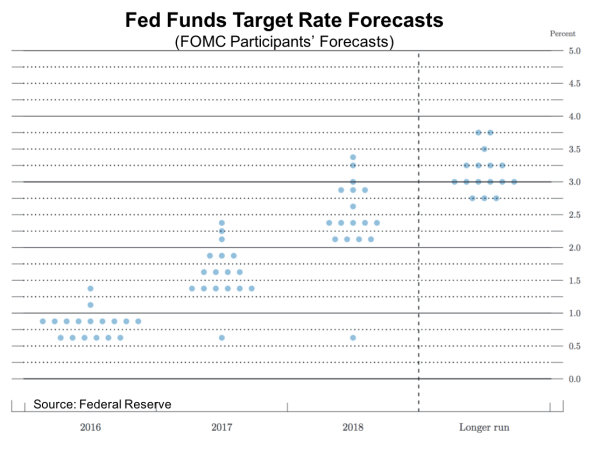

The Federal Reserve does not act again (although it is still expecting to do so in 2016) while manufacturing takes another break.

There are many jobs openings on the market. Unfortunately, employers are not filling those positions.