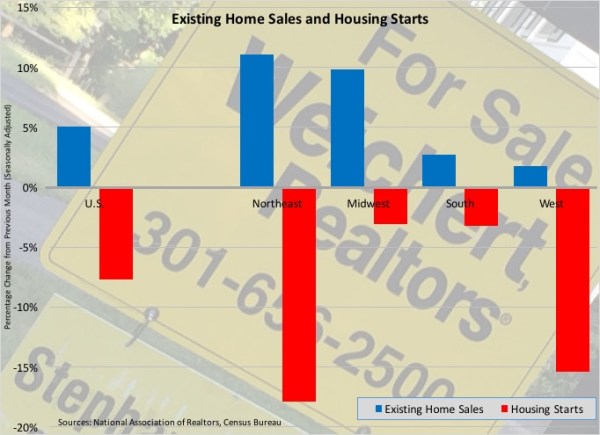

Economic activity remained slow in March, even though existing home sales bounced back.

Bounce in Housing, Economic Activity Wobbles: What We Learned During the Week of April 18-22

What We Learned About the U.S. Economy Last Week

Weekly Economic Update: A brief, non-technical review of the previous week's U.S. economic data releases by Kevin A. Roth, PhD

Economic activity remained slow in March, even though existing home sales bounced back.

Spring weather blossomed across parts of the U.S. last week, the same could not be said about data released last week on either industrial production or retail sales.

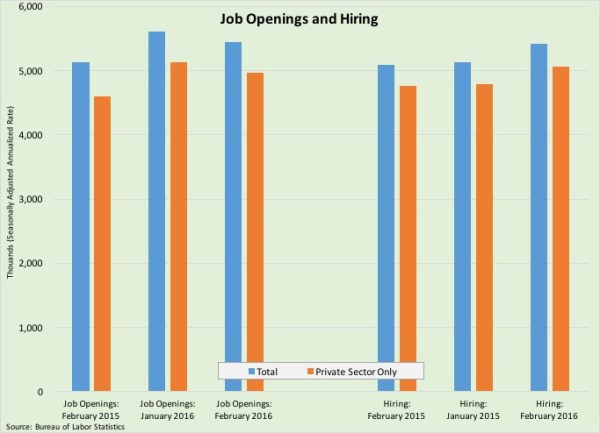

The labor market remains a bright spot as hiring jumped to a post-recession high during February. Meanwhile, global demand for U.S. goods weighed on the trade deficit.