Late 2019 data continued to signal sluggish growth.

Signs Point to Sluggish Growth: January 20 – 24

What We Learned About the U.S. Economy Last Week

Weekly Economic Update: A brief, non-technical review of the previous week's U.S. economic data releases by Kevin A. Roth, PhD

Late 2019 data continued to signal sluggish growth.

Retail sales ended 2019 on a positive note while job openings fell sharply.

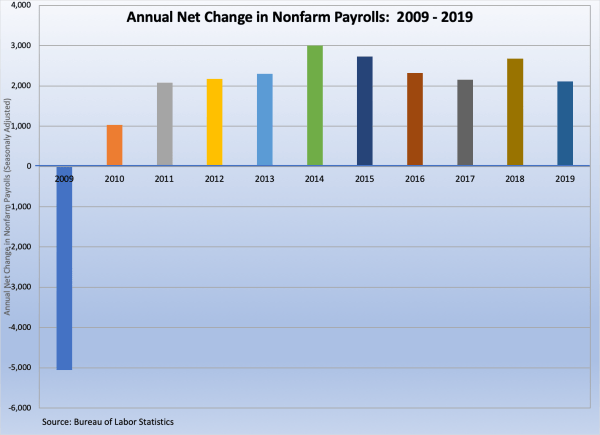

The U.S. labor market added 22.6 million jobs during the 2010s.